- Joined

- Oct 7, 2012

- Messages

- 5,228

- Points

- 113

The Singapore dollar is poised to weaken further as the escalating trade war between the world’s two largest economies weighs down growth in the export-dependent city-state.

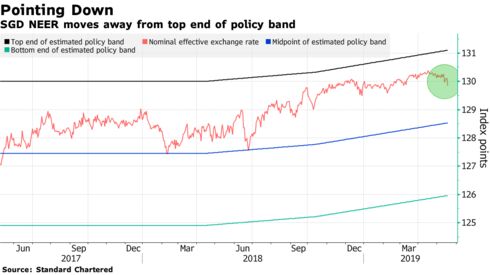

Poor export data that landed Friday underscore the downward pressure on the currency’s nominal effective exchange rate, which has quietly crept away from the upper end of the band that monetary policy makers use to keep Singapore on an even keel.

With no deal in sight between the U.S. and China, revised gross domestic product figures due Tuesday are the next thing to watch for clues on the trajectory of the Singapore dollar, which has slipped about 1% this month.

“Given the small size of the Singapore economy and the subdued outlook in the electronic sector, risk is for more weak economic data to come,” said Frances Cheung, head of Asia macro strategy at Westpac Banking Corp. “Potentially weak data may push MAS expectations toward a more dovish side.”

Larger declines in other Asian currencies caught in the crossfire between China and the U.S. has deflected attention from the simmering signs of weakness in the Singapore dollar. A closer look shows that six-month forward discounts on the greenback against the currency narrowed to the tightest level in 16 months last week.

The Singapore dollar fell 0.2 percent against to trade at S$1.3749 per U.S. dollar as of 3:58 p.m. local time on Friday.

The International Monetary Fund warns that the risks to the economy are tilted to the downside and that the Monetary Authority of Singapore’s response to the challenge should be "data dependent."

Cold Comfort

Analysts forecast a modest upward revision in first-quarter GDP growth to 1.5%, which would still leave it far below the five-year average of 2.9% and offer little support for the currency.

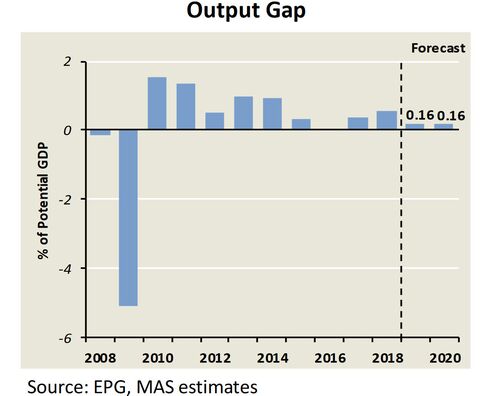

Looking beyond Tuesday’s data, a projected narrowing in the so-called output gap this year is also likely to keep inflationary pressures in check and weigh on the Singapore dollar.

The MAS said last month that economic output is currently running above the city-state’s potential rate but that the gap will narrow. The authority reduced the pace of currency gains twice 2015 before the output gap nearly closed the following year.

This is fanning speculation that policy makers may do the same again in their next policy decision in October.

MAS forecasts the output gap will narrow in its Macroeconomic Review report in April.

https://www.bloomberg.com/news/arti...-slipping-as-trade-war-chips-at-monetary-band

Poor export data that landed Friday underscore the downward pressure on the currency’s nominal effective exchange rate, which has quietly crept away from the upper end of the band that monetary policy makers use to keep Singapore on an even keel.

With no deal in sight between the U.S. and China, revised gross domestic product figures due Tuesday are the next thing to watch for clues on the trajectory of the Singapore dollar, which has slipped about 1% this month.

“Given the small size of the Singapore economy and the subdued outlook in the electronic sector, risk is for more weak economic data to come,” said Frances Cheung, head of Asia macro strategy at Westpac Banking Corp. “Potentially weak data may push MAS expectations toward a more dovish side.”

Larger declines in other Asian currencies caught in the crossfire between China and the U.S. has deflected attention from the simmering signs of weakness in the Singapore dollar. A closer look shows that six-month forward discounts on the greenback against the currency narrowed to the tightest level in 16 months last week.

The Singapore dollar fell 0.2 percent against to trade at S$1.3749 per U.S. dollar as of 3:58 p.m. local time on Friday.

The International Monetary Fund warns that the risks to the economy are tilted to the downside and that the Monetary Authority of Singapore’s response to the challenge should be "data dependent."

Cold Comfort

Analysts forecast a modest upward revision in first-quarter GDP growth to 1.5%, which would still leave it far below the five-year average of 2.9% and offer little support for the currency.

Looking beyond Tuesday’s data, a projected narrowing in the so-called output gap this year is also likely to keep inflationary pressures in check and weigh on the Singapore dollar.

The MAS said last month that economic output is currently running above the city-state’s potential rate but that the gap will narrow. The authority reduced the pace of currency gains twice 2015 before the output gap nearly closed the following year.

This is fanning speculation that policy makers may do the same again in their next policy decision in October.

MAS forecasts the output gap will narrow in its Macroeconomic Review report in April.

https://www.bloomberg.com/news/arti...-slipping-as-trade-war-chips-at-monetary-band