Though FTX Bankman-Fried, 30, was released last Thursday on a US$250 million (S$337 million) bond, he and the inner circle will be locked up as I do not see that they can influence markets anymore.

-

IP addresses are NOT logged in this forum so there's no point asking. Please note that this forum is full of homophobes, racists, lunatics, schizophrenics & absolute nut jobs with a smattering of geniuses, Chinese chauvinists, Moderate Muslims and last but not least a couple of "know-it-alls" constantly sprouting their dubious wisdom. If you believe that content generated by unsavory characters might cause you offense PLEASE LEAVE NOW! Sammyboy Admin and Staff are not responsible for your hurt feelings should you choose to read any of the content here. The OTHER forum is HERE so please stop asking.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Cryptocurrencies, tokens, NFTs, virtual "assets" frauds

- Thread starter LITTLEREDDOT

- Start date

FTX customers file class action lawsuit to lay claim to dwindling assets

The proposed class seeks a declaration that traceable customer assets are not FTX property. PHOTO: REUTERS

Dec 28, 2022

WILMINGTON, Delaware - FTX customers filed a class action lawsuit against the failed crypto exchange and its former top executives including Sam Bankman-Fried on Tuesday, seeking a declaration that the company’s holdings of digital assets belong to customers.

The lawsuit is the latest legal effort to lay claim to the dwindling assets of FTX, which is already feuding with liquidators in the Bahamas and Antigua as well as the bankruptcy estate of Blockfi, another failed crypto company.

FTX pledged to segregate customer accounts and instead allowed them to be misappropriated and therefore customers should be repaid first, according to the lawsuit filed in US Bankruptcy Court in Delaware.

“Customer class members should not have to stand in line along with secured or general unsecured creditors in these bankruptcy proceedings just to share in the diminished estate assets of the FTX Group and Alameda,” said the complaint.

Bahamas-based FTX halted withdrawals last month and filed for bankruptcy after customers rushed to pull their holdings from the what was once the second-largest cryptocurrency exchange after questions surfaced about its finances.

Bankman-Fried faces charges stemming from what a federal prosecutor called a “fraud of epic proportions” that included allegedly using customer funds to support his Alameda Research crypto trading platform.

Bankman-Fried has acknowledged risk-management failures at FTX but said he does not believe he has criminal liability. He has not yet entered a plea and was released on a US$250 million (S$337 million) bond last week that included restrictions on his travel.

The proposed class, which wants to represent more than 1 million FTX customers in the United States and abroad, seeks a declaration that traceable customer assets are not FTX property. The customer class also wants the court to find specifically that property held at Alameda that is traceable to customers is not Alameda property, according to the complaint.

The lawsuit seeks a declaration from the court that funds held in FTX US accounts for US customers and in FTX Trading accounts for non-US customers or other traceable customer assets are not FTX property. The customer class also wants the court to find specifically that property held at Alameda that is traceable to customers is not Alameda property, according to the complaint.

If the court determines it is FTX property, then the customers seek a ruling that they have a priority right to repayment over other creditors.

Crypto companies are lightly regulated and often based outside the US and deposits are not guaranteed as US bank and brokerage deposits are, complicating the question of whether the company or customers own the deposits. REUTERS

I grew my cryptocurrency portfolio by 8 times. Then I blew it on a scam

Sajid Ikram had made a bundle in cryptocurrency, so when he met a ‘cryptocurrency analyst’ on Facebook with a winning trading strategy, he didn’t think it would be a scam. It turned out to be an elaborate one.

Sajid Ikram had made big gains in cryptocurrency - but he lost it all to an elaborate scam. (Photo: Sajid Ikram)

26 Dec 2022

Sajid Ikram, 49, is an IT entrepreneur living in Canada. This is an edited version of his story, as told to CNA Insider.

EDMONTON, Canada: Actually, the scammers didn’t reach out to me first. I was the one who added one of them.

It all started in August last year when Facebook recommended a Nydia Chen to me as one of the “people you may know”. And I’m like, “Why does Facebook think I should connect with this person?”

To find out, I added her as a friend.

We chatted a little via Facebook and, when I asked her what she did, she replied that she was a cryptocurrency analyst. That’s probably why Facebook connected us.

I live in Edmonton, Canada, and I’ve been in the technology industry my whole life. I started dabbling in crypto in 2017, but only got into it properly at the end of 2020, when the whole scene started heating up.

I started with maybe C$30,000 (S$30,800) and by May or June last year, my portfolio was worth about eight times that.

It was around this time when there was a crypto crash. I was keeping my coins in a ledger wallet but because things move fast in crypto, I needed my coins available and easier to move.

At the time I met Nydia, I was looking to either take out some money or find a way to grow my portfolio more. You could say I was vulnerable.

THE FIRST PROFITS

Nydia told me she lived in Vancouver. She was an attractive woman, but I wasn’t looking for romance — I was happily married. It was clear to me that she wasn’t interested in me in that way either.She seemed a very private person. She wasn’t very flashy and didn’t like to chat about herself much. Now and then, she revealed glimpses of her personal life, like the time she was going to buy a house and asked me what I thought of it, or the time she made some dumplings.

But most of the time, we chatted about crypto. She told me she’d created a system of trading that she’d used for more than two years and that was about 80 per cent accurate.

I asked her to show me her strategy on the crypto exchange, Binance. But she told me she was unfamiliar with it. Instead, she used this other platform: Antsex.com.

“You’re not familiar with Binance, the biggest crypto exchange in the world?” I thought, incredulous. Besides, I’d never heard of Antsex.com, and I told her that.

She didn’t seem surprised at my response. She said the platform was popular with the Chinese community and was in fact an Ant Group company, but it wasn’t allowed to say that because the Chinese government might shut it down.

I’d heard of the Alibaba-affiliated Ant Group, and this sounded plausible at the time.

In the end, she persuaded me to try putting in US$5,000 (S$6,900). It was just a small part of my portfolio. I created an account, logged on, and she guided me through the process.

Our first trading session lasted an hour; in that time, my money doubled. Of course, I told my wife. And when Nydia told me to take out US$1,000 and treat my wife to a good dinner to celebrate, I did just that.

‘WE HAVE AN EDGE, RIGHT?’

Nydia told me to pledge, or stake, the rest of the profits to ANTC, a token on the platform.I’d been doing staking — locking up crypto assets in exchange for daily interest — with some of my other coins. But the returns from ANTC were amazing in comparison.

Nydia told me it wasn’t a mainstream token and wasn’t listed on other exchanges. Once it was listed, she said, the value would go through the roof.

“This is my gift to you,” she told me.

She said the investment strategy should be to keep enough money in my trading account — so it’d be available if the opportunity to trade came up — and keep the rest in ANTC because it was a “safe” investment that not only paid good interest but also was increasing in value.

I’d seen the value of a token go from US$0.10 to US$1.50 on the first day of trading on other exchanges like Binance, so I knew this could happen.

I was excited to be a part of this, so two weeks later, I put another US$10,000 in for a trading session. Again, I was able to take out some money, and pledge the rest of the profits.

In total, I’d put in US$15,000, but the platform showed that my account had more than US$100,000. This meant the token had appreciated a lot, and the investment was doing well.

It was around this time that Nydia highlighted the benefits the platform provided to people who make an appointment — a commitment to deposit a large sum of money. If I were to deposit US$100,000, for example, I’d get a 10 per cent bonus in USDT, a type of crypto.

“You’re expected to lose money on the platform,” she said. “But of course, we have an edge, right?”

It was a very attractive offer, and she told me I should take advantage of it. Besides, she said, we’d be trading in USDT (which is supposed to be pegged to the United States dollar), so if crypto crashed again, I’d be insulated (in theory).

So I started selling crypto in my existing portfolio. One of my largest holdings, at nearly US$100,000, was my Cardano crypto. I was waiting for the crypto to hit US$4 — it was worth almost US$3 at the time — but Nydia told me to sell it all. She told me it’d never even hit US$3.

I listened to her, and she was right. Its value went down fast after that point. I was so proud of my decision. There were at least three other times when she’d advised me on these things, and each time she was spot on.

There was no way she’d have been able to manipulate the overall crypto markets. She knew where things were headed, to my mind, so I decided to trust her and I made that appointment.

SHE CONVINCED ME IT WASN’T A SCAM

Before I deposited the money, I had to check out the platform again.I saw a Reddit post that said the platform was part of a romance scam, with posters talking about an attractive Chinese woman and how they couldn’t get their money out after depositing it. I couldn’t find much information about the platform besides this.

I panicked. I needed to get my money out. But I couldn’t make any withdrawals.

So I chatted with the site’s customer service via WhatsApp. They told me my account would be frozen until the appointment was completed. They explained that this was so that they’d know I’d be depositing new funds.

This sounded fair to me. But when I asked if I could withdraw my appointment, they told me my account would be permanently frozen, and they’d sue me for breach of contract. That freaked me out.

“Don’t believe what you read,” she also told me. “Everyone’s competing for customers — it could well be Binance that planted this story on Reddit.”I should’ve walked away there and then. Instead, I consulted Nydia. And she convinced me that the only way to resolve this was to go ahead and complete the appointment.

It sounded plausible to me, maybe because I was worried about what would happen if I didn’t pull the trigger. I took a deep breath and deposited that US$100,000.

I GOT MY FRIENDS INVOLVED

Within the next month or so, I transferred the remainder of my portfolio to the account. I thought the crypto that I had wasn’t going to go up much more, and I wanted to continue growing my money.Indeed, I saw the value of my investment rise to more than US$750,000. It may seem a ridiculous amount, but to me, it wasn’t anything out of the ordinary. I’d made huge amounts of money from cryptocurrency before.

I was also still able to make withdrawals; up to this point, I’d taken out close to C$75,000 (S$77,500).

I told them I was doing something risky, and they could lose everything, so they should do it only if they have the money.Then Nydia asked me to get my friends involved, to help them in the same way she was helping me.

My friends wanted me to prove that I could successfully withdraw money from the platform. So I withdrew US$50,000 to show them that it worked, then I put it back in.

Three of my friends put in a total of C$71,000. The value of the coin kept going up, and the numbers kept growing in the account.

Then in October 2021, Nydia tried to persuade me to make a second appointment, this time for US$200,000. She told me it was time to move to the next level of trading, and the bonus for the deposit would help me get to the amount required to hit that level.

All my liquid capital was already on the platform, so Nydia suggested I borrow from other friends and pay them back with 10 per cent interest after a month. She said the profits would be way more than 10 per cent, and my friends were going to profit themselves, just by helping me out.

I put in C$25,000 of the money I’d taken out previously and borrowed about C$100,000 from another friend. The three friends who’d earlier invested put in another C$30,000. But it wasn’t enough to make the appointment, so Nydia lent me the rest, which she sent to me on the platform.

Each time I asked my friends for money, I was upfront about why I needed it. They knew what I was up to and had seen my gains previously. One of my three initial friends sent me another C$50,000 after I completed the appointment. I put it in the platform anyway.

EVERYTHING BLEW UP

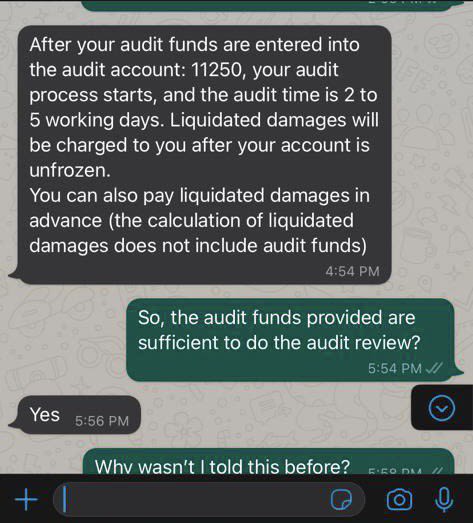

By last November, the value of my account was more than US$1 million. I wanted to withdraw US$200,000, the largest withdrawal I could make at a time, according to the site’s customer service. I wanted to pay my friends back.They added that I’d triggered the platform’s audit mechanism by making too many transactions, and I needed to deposit fresh funds — 15 per cent of the account balance, or approximately US$220,000 — within three days so they could test the security of the flow of funds into my account.But it didn’t work. Customer service told me my account had been permanently frozen and was being investigated for fraud.

Once the audit had passed, they would deposit the money. I negotiated with them, and they agreed to let me pay about US$10,000 first. The rest, they said, would be due in seven days, after which my account would lapse.

I think it was when I heard this that it finally hit me that I’d been scammed. That was when everything blew up. I couldn’t sleep and was on edge all the time, just worrying about the money.

And my marriage was rather strained. My wife had known all along that I was trading, but I’d promised her that I wouldn’t borrow money from other people. But I did, so there are now trust issues in my marriage.

I wanted to continue chatting to Nydia to see if I could learn anything about the scam or figure out where the scammers were so that I’d have more information before I went to the police. But my wife insisted that I block her.

“This person is getting under your skin,” she told me. “She’s brainwashed you.”

I haven’t chatted to Nydia since then, and I haven’t been looking for her. She might still be out there, but I wouldn’t know.

THE FALLOUT, AND SOME RED FLAGS

I lost more than C$450,000, more than half of which was my friends’ money. It wasn’t easy telling them their money was gone.I’m selling a piece of land that was meant to be my inheritance, so I can pay some of my friends back. That’s a bitter pill to swallow.

As for my marriage, things are better now. It takes years to build trust and you can ruin it in a minute. I think this is going to hang over our relationship for a long time.

I was in therapy for a while, and I think I’ve been able to deal with it.

Part of my therapy involved volunteering for the Global Anti-Scam Organisation (Gaso). I help with its website, talk to some scam victims and share my story as much as possible to raise awareness about pig-butchering scams (involving bogus investments).

I created a website called Stopascammer.com — with information on how to spot such scams and how they work — to help other people who’ve been scammed. Just maybe, we can find these scammers. (I’ve since merged it with Gaso’s services.)

Previous

This is what I tell people to look out for: Firstly, look up the domain name to see when it was registered. In many cases, it may have been registered within a year or even months before you came across it.

Secondly, if there’s a WhatsApp or online customer service chat to make withdrawals or deposits, that’s a dead giveaway.

Thirdly, it may be a super slick website, but look at their terms of service — you may find inconsistencies and spelling or grammatical errors there.

But the most important piece of advice I’d give a friend is: These kinds of profits don’t happen with a stranger you met on the internet.

Yes, I experienced dramatic gains myself in the crypto world. But that comes from learning and talking to some friends. Sometimes your friends are right, sometimes they’re wrong, but a stranger on the internet chatting to you is never right.

Text: Lianne Chia

another crypto sexchange to bite the dust?

https://www.yahoo.com/finance/news/crypto-exchange-gemini-sued-investors-132406586.html

https://www.yahoo.com/finance/news/crypto-exchange-gemini-sued-investors-132406586.html

but, but he's broke!! no money left!! less than $100k in his accounts!!Though FTX Bankman-Fried, 30, was released last Thursday on a US$250 million (S$337 million) bond, he and the inner circle will be locked up as I do not see that they can influence markets anymore.

oh by the way, I'm posting my 250million bond...

@syed putra . don't fall for it ok?I grew my cryptocurrency portfolio by 8 times. Then I blew it on a scam

Sajid Ikram had made a bundle in cryptocurrency, so when he met a ‘cryptocurrency analyst’ on Facebook with a winning trading strategy, he didn’t think it would be a scam. It turned out to be an elaborate one.

Sajid Ikram had made big gains in cryptocurrency - but he lost it all to an elaborate scam. (Photo: Sajid Ikram)

26 Dec 2022

Sajid Ikram, 49, is an IT entrepreneur living in Canada. This is an edited version of his story, as told to CNA Insider.

EDMONTON, Canada: Actually, the scammers didn’t reach out to me first. I was the one who added one of them.

It all started in August last year when Facebook recommended a Nydia Chen to me as one of the “people you may know”. And I’m like, “Why does Facebook think I should connect with this person?”

To find out, I added her as a friend.

We chatted a little via Facebook and, when I asked her what she did, she replied that she was a cryptocurrency analyst. That’s probably why Facebook connected us.

I live in Edmonton, Canada, and I’ve been in the technology industry my whole life. I started dabbling in crypto in 2017, but only got into it properly at the end of 2020, when the whole scene started heating up.

I started with maybe C$30,000 (S$30,800) and by May or June last year, my portfolio was worth about eight times that.

It was around this time when there was a crypto crash. I was keeping my coins in a ledger wallet but because things move fast in crypto, I needed my coins available and easier to move.

At the time I met Nydia, I was looking to either take out some money or find a way to grow my portfolio more. You could say I was vulnerable.

THE FIRST PROFITS

Nydia told me she lived in Vancouver. She was an attractive woman, but I wasn’t looking for romance — I was happily married. It was clear to me that she wasn’t interested in me in that way either.

She seemed a very private person. She wasn’t very flashy and didn’t like to chat about herself much. Now and then, she revealed glimpses of her personal life, like the time she was going to buy a house and asked me what I thought of it, or the time she made some dumplings.

But most of the time, we chatted about crypto. She told me she’d created a system of trading that she’d used for more than two years and that was about 80 per cent accurate.

A picture of the house “Nydia” sent Sajid, asking him what he thought about it. (Photo: Sajid Ikram)

I asked her to show me her strategy on the crypto exchange, Binance. But she told me she was unfamiliar with it. Instead, she used this other platform: Antsex.com.

“You’re not familiar with Binance, the biggest crypto exchange in the world?” I thought, incredulous. Besides, I’d never heard of Antsex.com, and I told her that.

She didn’t seem surprised at my response. She said the platform was popular with the Chinese community and was in fact an Ant Group company, but it wasn’t allowed to say that because the Chinese government might shut it down.

I’d heard of the Alibaba-affiliated Ant Group, and this sounded plausible at the time.

In the end, she persuaded me to try putting in US$5,000 (S$6,900). It was just a small part of my portfolio. I created an account, logged on, and she guided me through the process.

Our first trading session lasted an hour; in that time, my money doubled. Of course, I told my wife. And when Nydia told me to take out US$1,000 and treat my wife to a good dinner to celebrate, I did just that.

‘WE HAVE AN EDGE, RIGHT?’

Nydia told me to pledge, or stake, the rest of the profits to ANTC, a token on the platform.

I’d been doing staking — locking up crypto assets in exchange for daily interest — with some of my other coins. But the returns from ANTC were amazing in comparison.

Nydia told me it wasn’t a mainstream token and wasn’t listed on other exchanges. Once it was listed, she said, the value would go through the roof.

“This is my gift to you,” she told me.

She said the investment strategy should be to keep enough money in my trading account — so it’d be available if the opportunity to trade came up — and keep the rest in ANTC because it was a “safe” investment that not only paid good interest but also was increasing in value.

I’d seen the value of a token go from US$0.10 to US$1.50 on the first day of trading on other exchanges like Binance, so I knew this could happen.

I was excited to be a part of this, so two weeks later, I put another US$10,000 in for a trading session. Again, I was able to take out some money, and pledge the rest of the profits.

In total, I’d put in US$15,000, but the platform showed that my account had more than US$100,000. This meant the token had appreciated a lot, and the investment was doing well.

It was around this time that Nydia highlighted the benefits the platform provided to people who make an appointment — a commitment to deposit a large sum of money. If I were to deposit US$100,000, for example, I’d get a 10 per cent bonus in USDT, a type of crypto.

“You’re expected to lose money on the platform,” she said. “But of course, we have an edge, right?”

Details of the “appointment” — and the attractive benefits available to those who took advantage of it. (Photo: Sajid Ikram)

It was a very attractive offer, and she told me I should take advantage of it. Besides, she said, we’d be trading in USDT (which is supposed to be pegged to the United States dollar), so if crypto crashed again, I’d be insulated (in theory).

So I started selling crypto in my existing portfolio. One of my largest holdings, at nearly US$100,000, was my Cardano crypto. I was waiting for the crypto to hit US$4 — it was worth almost US$3 at the time — but Nydia told me to sell it all. She told me it’d never even hit US$3.

I listened to her, and she was right. Its value went down fast after that point. I was so proud of my decision. There were at least three other times when she’d advised me on these things, and each time she was spot on.

There was no way she’d have been able to manipulate the overall crypto markets. She knew where things were headed, to my mind, so I decided to trust her and I made that appointment.

He started selling off the crypto in his existing portfolio — and “Nydia”’s advice seemed to be spot on. (Photo: iStock)

SHE CONVINCED ME IT WASN’T A SCAM

Before I deposited the money, I had to check out the platform again.

I saw a Reddit post that said the platform was part of a romance scam, with posters talking about an attractive Chinese woman and how they couldn’t get their money out after depositing it. I couldn’t find much information about the platform besides this.

I panicked. I needed to get my money out. But I couldn’t make any withdrawals.

So I chatted with the site’s customer service via WhatsApp. They told me my account would be frozen until the appointment was completed. They explained that this was so that they’d know I’d be depositing new funds.

This sounded fair to me. But when I asked if I could withdraw my appointment, they told me my account would be permanently frozen, and they’d sue me for breach of contract. That freaked me out.

“Don’t believe what you read,” she also told me. “Everyone’s competing for customers — it could well be Binance that planted this story on Reddit.”

It sounded plausible to me, maybe because I was worried about what would happen if I didn’t pull the trigger. I took a deep breath and deposited that US$100,000.

I GOT MY FRIENDS INVOLVED

Within the next month or so, I transferred the remainder of my portfolio to the account. I thought the crypto that I had wasn’t going to go up much more, and I wanted to continue growing my money.

Indeed, I saw the value of my investment rise to more than US$750,000. It may seem a ridiculous amount, but to me, it wasn’t anything out of the ordinary. I’d made huge amounts of money from cryptocurrency before.

I was also still able to make withdrawals; up to this point, I’d taken out close to C$75,000 (S$77,500).

I told them I was doing something risky, and they could lose everything, so they should do it only if they have the money.

My friends wanted me to prove that I could successfully withdraw money from the platform. So I withdrew US$50,000 to show them that it worked, then I put it back in.

Three of my friends put in a total of C$71,000. The value of the coin kept going up, and the numbers kept growing in the account.

Sajid said he was upfront with his friends about why he needed the money. (Photo: iStock)

Then in October 2021, Nydia tried to persuade me to make a second appointment, this time for US$200,000. She told me it was time to move to the next level of trading, and the bonus for the deposit would help me get to the amount required to hit that level.

All my liquid capital was already on the platform, so Nydia suggested I borrow from other friends and pay them back with 10 per cent interest after a month. She said the profits would be way more than 10 per cent, and my friends were going to profit themselves, just by helping me out.

I put in C$25,000 of the money I’d taken out previously and borrowed about C$100,000 from another friend. The three friends who’d earlier invested put in another C$30,000. But it wasn’t enough to make the appointment, so Nydia lent me the rest, which she sent to me on the platform.

Each time I asked my friends for money, I was upfront about why I needed it. They knew what I was up to and had seen my gains previously. One of my three initial friends sent me another C$50,000 after I completed the appointment. I put it in the platform anyway.

EVERYTHING BLEW UP

By last November, the value of my account was more than US$1 million. I wanted to withdraw US$200,000, the largest withdrawal I could make at a time, according to the site’s customer service. I wanted to pay my friends back.

They added that I’d triggered the platform’s audit mechanism by making too many transactions, and I needed to deposit fresh funds — 15 per cent of the account balance, or approximately US$220,000 — within three days so they could test the security of the flow of funds into my account.

Once the audit had passed, they would deposit the money. I negotiated with them, and they agreed to let me pay about US$10,000 first. The rest, they said, would be due in seven days, after which my account would lapse.

The platform's customer service told Sajid he needed to deposit fresh funds after he triggered the platform's audit mechanism. (Photo: Sajid Ikram)

I think it was when I heard this that it finally hit me that I’d been scammed. That was when everything blew up. I couldn’t sleep and was on edge all the time, just worrying about the money.

And my marriage was rather strained. My wife had known all along that I was trading, but I’d promised her that I wouldn’t borrow money from other people. But I did, so there are now trust issues in my marriage.

I wanted to continue chatting to Nydia to see if I could learn anything about the scam or figure out where the scammers were so that I’d have more information before I went to the police. But my wife insisted that I block her.

“This person is getting under your skin,” she told me. “She’s brainwashed you.”

I haven’t chatted to Nydia since then, and I haven’t been looking for her. She might still be out there, but I wouldn’t know.

THE FALLOUT, AND SOME RED FLAGS

I lost more than C$450,000, more than half of which was my friends’ money. It wasn’t easy telling them their money was gone.

I’m selling a piece of land that was meant to be my inheritance, so I can pay some of my friends back. That’s a bitter pill to swallow.

As for my marriage, things are better now. It takes years to build trust and you can ruin it in a minute. I think this is going to hang over our relationship for a long time.

I was in therapy for a while, and I think I’ve been able to deal with it.

Part of my therapy involved volunteering for the Global Anti-Scam Organisation (Gaso). I help with its website, talk to some scam victims and share my story as much as possible to raise awareness about pig-butchering scams (involving bogus investments).

I created a website called Stopascammer.com — with information on how to spot such scams and how they work — to help other people who’ve been scammed. Just maybe, we can find these scammers. (I’ve since merged it with Gaso’s services.)

Previous

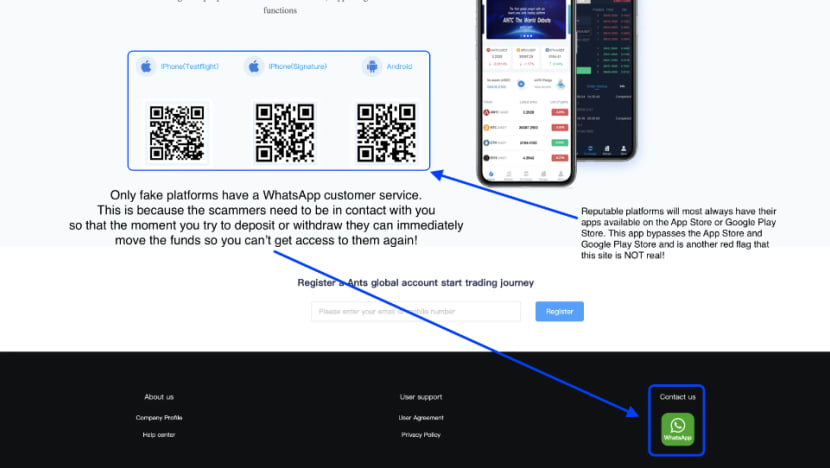

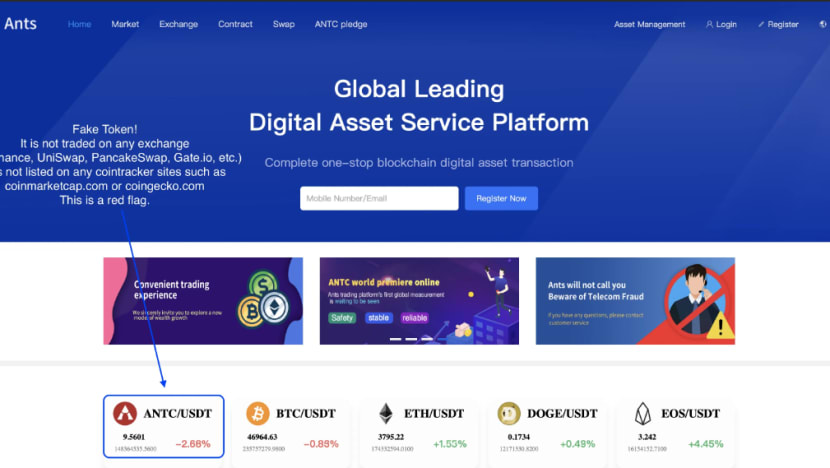

In hindsight, the red flags on the platform. Sajid uploaded these - together with his warnings - on the Stopascammer.com website.In hindsight, the red flags on the platform. Sajid uploaded these - together with his warnings - on the Stopascammer.com website. (Photos: Sajid Ikram)In hindsight, the red flags on the platform. Sajid uploaded these - together with his warnings - on the Stopascammer.com website.In hindsight, the red flags on the platform. Sajid uploaded these - together with his warnings - on the Stopascammer.com website. (Photos: Sajid Ikram)In hindsight, the red flags on the platform. Sajid uploaded these - together with his warnings - on the Stopascammer.com website.

This is what I tell people to look out for: Firstly, look up the domain name to see when it was registered. In many cases, it may have been registered within a year or even months before you came across it.

Secondly, if there’s a WhatsApp or online customer service chat to make withdrawals or deposits, that’s a dead giveaway.

Thirdly, it may be a super slick website, but look at their terms of service — you may find inconsistencies and spelling or grammatical errors there.

But the most important piece of advice I’d give a friend is: These kinds of profits don’t happen with a stranger you met on the internet.

Yes, I experienced dramatic gains myself in the crypto world. But that comes from learning and talking to some friends. Sometimes your friends are right, sometimes they’re wrong, but a stranger on the internet chatting to you is never right.

Text: Lianne Chia

THE WHOLE WORLD MAY THINK INFORMATION TECHNOLOGY IS GOOD

GOOD, I do not dispute

But it is used as a weapon of mass destruction.

Similar to the Atomic or Nuclear energy,

Instead of using them for constructive purposes,

INTERNET, digital transformation and CLOUD automation are being USED for destructive purposes

GOOD, I do not dispute

But it is used as a weapon of mass destruction.

Similar to the Atomic or Nuclear energy,

Instead of using them for constructive purposes,

INTERNET, digital transformation and CLOUD automation are being USED for destructive purposes

Two Torque employees declared bankrupt over millions in misappropriated cryptocurrencies

The former employees had conspired to misappropriate more than US$479 million (S$642 million) worth of cryptocurrency assets. PHOTO: TORQUE TRADING SYSTEM/FACEBOOK

Joyce Lim

Senior Correspondent

Dec 30, 2022

SINGAPORE – Two former senior employees of failed cryptocurrency trading platform Torque were declared bankrupt on Thursday, after the company’s liquidators began bankruptcy proceedings against them in relation to hundreds of millions worth of stolen cryptocurrencies.

Court documents revealed that Torque’s former chief product officer, Mr Fong Chee Kiong, 39, had conspired with its former chief technology officer, Mr Wu Zhong Yee, 39, to misappropriate more than US$479 million (S$642 million) worth of cryptocurrency assets from Torque between January 2020 and February 2021.

The stolen cryptocurrencies were transferred from Torque’s accounts to digital wallets and accounts belonging to the defendants, some of which were held with cryptocurrency exchange Binance.

Both men were operating out of Vietnam and had sole access to Torque’s digital wallets.

Torque, which was founded by Singaporean Bernard Ong and wound up in 2021, was incorporated in the British Virgin Islands (BVI), with management in Singapore and operations in Vietnam. Mr Ong, its sole shareholder, also served as its director and chief executive.

About 3,500 of its 17,700 users in 120 countries are Singaporeans or investors based here, with total cryptocurrency assets valued at about US$124 million.

In February 2021, Mr Ong made a police report against Mr Wu, also known as Zee, for conducting unauthorised trades resulting in significant losses of investor funds. Mr Ong then applied to the BVI courts to wind up the company.

He also alleged that Mr Wu had made an unauthorised withdrawal of 72 bitcoins from Torque‘s Binance account on Feb 7, 2021. These could have been worth more than US$4 million at certain points that month.

Investigations later revealed that some time on or around Feb 7 that year, Mr Fong and/or Mr Wu had transferred the 72 bitcoins to a digital wallet that did not belong to Torque, without consent or authorisation from Torque.

Of the 72 bitcoins, about 13 were transferred and credited to Mr Fong’s Binance sub-accounts.

Torque’s liquidators, represented by lawyers Danny Ong, Yam Wern Jhien and Jansen Chow, had in early 2021 obtained default judgments against Mr Fong and Mr Wu.

The liquidators are seeking to recover more than US$363 million from Mr Wu and more than US$462 million from Mr Fong.

The team of lawyers proceeded with the bankruptcy applications and orders in 2022, based on the unsatisfied judgment debts.

Court documents revealed that several attempts were made to serve the statutory demands on both defendants via text messages, e-mails, and notices placed in The Straits Times.

On July 5, a copy of the statutory demand was also left at Mr Wu’s home in Pasir Ris. It was the lawyers’ second attempt at serving the documents.

On the first attempt, a woman who answered the door and identified herself as Mr Wu’s wife had said that Mr Wu was not at home and she did not know when he would be back.

Mr Wu and Mr Fong remain at large.

More than 70 police reports have been filed against Torque and Mr Ong, with investors claiming millions lost in cryptocurrencies.

The liquidators from restructuring and insolvency specialist Borrelli Walsh have said that they did not find any audited financial statements or reliable information from management accounts or any other account held by Torque on any other cryptocurrency exchange.

In May, Mr Ong was directed by the Singapore High Court to respond to the liquidators’ questions.

In a circular to creditors in June, Torque’s liquidators said that legal proceedings will be taken against some individuals through the BVI and Singapore courts as part of the liquidators’ planned recovery actions.

The legal claims would be broadly of the nature of breach of director’s duties and claims available under BVI law.

Depending on Mr Ong’s response, the liquidators said, they have the option of requiring Mr Ong to be examined personally in court.

Crypto is starting to be like another Clob saga

FTX founder Sam Bankman-Fried (centre) leaves a federal courthouse in New York, on Dec 22, 2022. The collapse of FTX has also hit local investors. PHOTO: EPA-EFE

David Gerald

Jan 1, 2023

The Securities Investors Association (Singapore) or Sias was born when a huge speculative segment of the local stock market known as Clob International – on which some 180 Malaysian stocks were traded over the counter – crashed spectacularly in 1998, leading to billions of dollars being lost by Singapore investors.

This occurred at the height of the Asian financial crisis, when the Malaysian government imposed capital controls on the ringgit, declared Clob to be an illegal market and ordered the migration of all Malaysian shares back to the Kuala Lumpur Stock Exchange, or KLSE.

Clob’s demise suddenly hit some 172,000 Singapore investors, among them retirees who lost their life savings as they invested almost entirely on rumour, speculation and hearsay, mostly from friends, family members and even acquaintances.

In other words, Clob was a market in which the value of most of the assets that were traded depended on hype, inflated expectations and, at the end of the day, how much the next fool was willing to pay.

Now, a little more than two decades later, we find ourselves reading about the billions that investors worldwide have lost because of the collapse of various cryptocurrencies.

More recently, the bankruptcy of FTX has also hit local investors. FTX was an external cryptocurrency exchange on which the assets that were traded relied on hype, inflated expectations and, let’s be honest, how much the next greater fool was willing to pay.

The similarities between the two crashes are striking. In both cases, greed, the herd instinct and the fear of missing out were the main reasons why investors took the plunge. There was no regard for fundamentals – in the case of Clob stocks, few had any, while in the case of cryptos, there aren’t any.

However, for Clob, there were at least KLSE listing rules and disclosure requirements to provide some semblance of regulation, while stockbroking research gave some basis for valuation. None of these safeguards currently exists for the crypto market.

Indeed, it is not hard to see why the vast majority of regulators and academics have likened it to a massive Ponzi scheme, built on nothing but empty promises.

For example, the dean of the London School of Economics and Political Science Andres Velasco in a recent article (“The unbearable uselessness of crypto”) said that “thanks to FTX, the world may have woken up to the grim reality that crypto is a get-rich-quick lie, wrapped in hype, bobbing on an ocean of libertarian technobabble”.

Speaking of technobabble, which essentially refers to the much-vaunted blockchain technology that is supposed to enable transactions outside of the traditional banking system, Nobel Prize-winning economist Paul Krugman has pointed out that cryptos have made no inroads as an alternative means of payment after 14 years of hype.

“Cryptocurrencies are largely purchased through exchanges like Coinbase and, yes, FTX, which take your money and hold crypto tokens in your name,” he wrote.

“These exchanges are – wait for it – financial institutions, whose ability to attract investors depends on – wait for it again – those investors’ trust. In other words, the crypto ecosystem has basically evolved into exactly what it was supposed to replace: a system of financial intermediaries whose ability to operate depends on their perceived trustworthiness.

“In which case, what is the point? Why should an industry that at best has simply reinvented conventional banking have any fundamental value?” wrote Professor Krugman.

By now, it is very likely that most – if not all – investors would know these arguments. They would also know that the official government stance here is that cryptos are wholly unsuitable for retail investors.

Yet there will be some who will still participate in the hope of getting rich quick. Instead of pressing on and continuing to try their luck – a path that is more likely than not to lead to financial disaster – why not learn from past mistakes and undertake investing according to tried and trusted principles?

Sias would like to offer these guidelines, derived from more than two decades of experience in the local financial market:

1. Do not allow greed to dominate your investment decisions

Make an informed decision. Invest with knowledge.2. Know your investment horizon

This refers to the length of time you have ahead of you to earn back losses and ride out short-term volatility. The mistake many retirees made during the Clob saga was ploughing their retirement money into massively speculative stocks, so when the crash came, not only were their life savings wiped out, but they also had no time to recover their losses.Older individuals should ideally have a greater proportion of their investment portfolio in safer instruments, such as high-grade bonds and blue-chip, dividend-paying stocks that can provide a regular stream of passive income. Younger investors, in the meantime, can take on more risk – provided their risk profiles allow them to.

All individuals, regardless of age, should also familiarise themselves with how to maximise the benefits of the Central Provident Fund, which is the national social security savings scheme that can provide a basic monthly income for life.

3. Invest according to your risk profile

It is important to know that this is made up of two components – risk tolerance and risk capacity. Risk tolerance refers to your emotional ability to take risk – whether you are a risk seeker or whether you are risk-averse.Risk capacity, on the other hand, refers to a person’s financial ability to take risk.

Someone who earns, say, $3,000 a month and has financial obligations like a housing loan may have a high risk tolerance but is limited in his ability to take risk by his risk capacity.

Similarly, someone might earn $10,000 a month and have a high risk capacity but could have a low risk tolerance.

4. Diversify to reduce risk

During Clob’s crash, Sias encountered a retiree who put $500,000 into a single stock and lost it all. She would have been much better off investing $100,000 each into five different counters; that way, a crash in one might not have led to her losing all her savings.5. Do your homework

Sias cannot emphasise enough the importance of understanding all the features of a product or stock under consideration, especially the associated risks.For instance, when failed water treatment company Hyflux issued high-yielding perpetuals and preference shares, few – if any – retail investors gave any consideration to the considerable risks involved; most were instead attracted to the high headline returns and thus threw caution to the wind.

6. Rebalance your portfolio as you age

A young investor in his or her 20s and 30s might hold a portfolio comprising 50 per cent high-risk assets, 30 per cent medium-risk and 20 per cent low-risk. As they enter their 40s and early 50s, they should reduce their high-risk holding to around 30 per cent while increasing their medium-risk proportion to 50 per cent.Then, when they enter their 60s, they should ideally be invested in less risky assets.

A possible asset allocation would be 10 per cent high-risk, 20 per cent medium-risk and 70 per cent low-risk.

All of the above are tried and trusted pillars of investing. Following them will not guarantee vast rewards, but investors will stand a much better chance of earning decent, albeit modest, returns while minimising the risk of loss. Which is more than can be said of punting cryptos.

So, little or nothing much has changed from Clob to crypto. So long as investors look only at returns and not at the risks, they will continue to collect tears and not dollars.

- The writer is the founding chief executive of Sias

Singapore-based crypto firm hit by Boxing Day hack, more than $10 million lost

Affected users were advised to update to version 7.3.0 of the BitKeep app, which was put out on Dec 28. SCREENGRAB: BITKEEP

Aqil Hamzah

Jan 4, 2023

SINGAPORE – More than US$8 million (S$10 million) was stolen from a Singapore-based crypto wallet provider last Monday after a hacker manipulated files enabling users to download the wallets on their phones.

Thousands of users reported having their funds stolen from their BitKeep wallets on Boxing Day, although it is not clear how many Singaporean users were affected.

According to blockchain security and data analytics company PeckShield, the cryptocurrencies stolen consisted of Binance’s BNB Coin, stablecoins Tether and Dai as well as Ether.

The Straits Times has contacted BitKeep for more information but multiple attempts to do so via email and social media have gone unanswered.

Efforts to pinpoint its office in Singapore or unique entity number yielded no results, and the firm did not have a listed phone number here.

In a statement on the Bitkeep website last Wednesday, BitKeep chief executive Kevin Como acknowledged the incident and said the hacker had done so by hijacking and installing code on version 7.2.9 of the APK files available for download on the website.

APK files allow Android users to download apps directly onto their devices without going through the Google Play Store.

“With maliciously implanted code, the altered APK led to the leak of user’s private keys and enabled the hacker to move funds,” Mr Como said, adding that users who downloaded the app from Apple’s App Store, the Google Play Store or Chrome Web Store were unaffected.

On its official Telegram channel, affected users were advised to update to version 7.3.0 of the BitKeep app, which was put out on Dec 28.

They would then need to create a new crypto wallet and transfer all their available assets over.

Meanwhile, the firm said it is working to recover the stolen funds, with affected users urged to fill in a Google form detailing the amount they lost.

ST understands that BitKeep did not apply for a licence to provide digital payment token services under the Payment Services Act. This means that its cryptocurrency wallet may not fall under the category of a regulated service in Singapore.

BitKeep is also not a notified entity, which means it has not been granted a temporary exemption from holding a licence by the Monetary Authority of Singapore.

This is not the first time that BitKeep, which claims to have more than 8 million users across 168 countries, has suffered from a hack resulting in stolen funds.

In Oct 2022, more than US$1 million was stolen after hackers exploited a vulnerability that allowed them to perform cryptocurrency token swaps from users’ accounts.

Crypto crime volume hits all-time high on the back of more sanctions

The illegal transactions range from human trafficking to ransomware, stolen funds, terrorism financing, scams, cyber crimes, fraud and the darknet market. PHOTO: REUTERS

Claire Huang

Business Correspondent

Jan 12, 2023

SINGAPORE - The volume of cryptocurrency-related crime hit a new high in 2022 on the back of more sanctioned entities, despite the digital asset market sell-off.

In what blockchain research firm Chainalysis said was a more conservative estimate, the illicit transaction volume went up to US$20.1 billion (S$26.7 billion) last year.

These illegal transactions include human trafficking, ransomware, stolen funds, terrorism financing, scams, cybercrimes, fraud and the Darknet market.

This is up from US$18 billion in 2021 – this figure was earlier estimated to be a lower US$14 billion.

The firm said in a report released on Thursday that the 2022 figure “is sure to grow over time as we identify new addresses associated with illicit activity”.

Chainalysis noted that the calculation does not include proceeds from non-crypto-native crimes, such as conventional drug trafficking that involves crypto as a mode of payment.

Of the illegal crypto transactions last year, 44 per cent came from activities linked to sanctioned entities, including Russian exchange Garantex, which accounted for the majority of transaction volume last year.

In a blog post on Monday, Chainalysis said the Office of Foreign Assets Control (Ofac) of the United States Department of the Treasury first issued crypto-related sanctions in 2018.

The number of sanctioned crypto-linked entities has grown from two in 2018 to 10 in 2022, in tandem with the rise in sanction-related addresses, which went up from two in 2018 to 350 in 2022.

Ofac sanctioned Garantex in April 2022 but, as a Russia-based business, the exchange has been able to continue operations.

“Transactions associated with Garantex or any other sanctioned crypto service represent, at the very least, substantial compliance risk for businesses that are subject to US jurisdiction, including fines and potential criminal charges,” the report said.

The report also found that the share of illegal activity among all crypto transactions has risen for the first time since 2019. It went up to 0.24 per cent in 2022, from 0.12 per cent in 2019.

The report said the rise should not come as a surprise, adding that it was expected as the total transaction volume fell with the onset of the bear market, while illicit transaction volume crept up.

Chainalysis said the increase in 2022 is significant as “the share corresponds with a very high value of economic value flows when expressed in US dollars – approximately US$20 billion in 2022 and US$18 billion in 2021”.

“These numbers, as we note, are a base case for the level of illicit activity on (the blockchain), and would not capture the use of crypto to facilitate physical-world drug exchange or other activities,” it added.

In the calculation of the overall share of illegal activity, Chainalysis said that it does not include volumes associated with centralised services that collapsed in 2022, some of which are facing charges of fraud, given the lack of off-chain insights.

Founders of failed crypto fund Three Arrows Capital looking to raise $33m for new venture

3AC’s Mr Zhu Su and Mr Kyle Davies, along with the co-founders of crypto exchange CoinFlex, have a new venture named GTX. PHOTO: REUTERS

Claire Huang

Business Correspondent

Jan 17, 2023

SINGAPORE – The two men behind bankrupt Three Arrows Capital (3AC) are looking for funding to stage a comeback, six months after their cryptocurrency hedge fund collapsed.

3AC’s Mr Zhu Su and Mr Kyle Davies – along with crypto exchange CoinFlex co-founders Mark Lamb and Sudhu Arumugam – are aiming to raise US$25 million (S$33 million) in seed funding to launch a platform for crypto bankruptcy claims that they have dubbed GTX.

Mr Zhu told The Straits Times on Monday night that the idea is to allow clients from bankrupt exchange FTX and other insolvent estates to access their capital and start investing again. “And being able to offer them stocks as well,” he said.

“We aim to verify and tokenise their claims and allow claims as collateral,” Mr Zhu said, when asked about how the platform would work.

Going by information leaked on Twitter, the name of the new firm references FTX, playing on the fact that the letter “G” comes after “F”.

The new outfit comes six months after 3AC collapsed and two months after the fall of Sam Bankman-Fried’s FTX.

3AC was set up in 2012 by Mr Zhu and Mr Davies, both Singapore citizens and aged 35.

The pair had attended United States high school Philips Academy and Columbia University together, and later worked as traders at Credit Suisse.

The two men said 3AC, registered in the British Virgin Islands, had more than US$4 billion in assets under management at its peak.

The prominent crypto fund was hit by the collapse of stablecoin TerraUSD and sister token Luna in May last year and the bankruptcy proceeding is playing out in Singapore as the country’s High Court has recognised the liquidation order from the British Virgin Islands court.

Reports over a week ago said the two co-founders, whose whereabouts are unclear, have received formal demands via Twitter from liquidators over how the hedge fund collapsed.

Mr Zhu had previously said in a December interview with ST that he toggles between Indonesia and the United Arab Emirates.

Of late, both Mr Zhu and Mr Davies have been active on social media and have publicly blamed Bankman-Fried, 30, of betting against 3AC’s position and dealing the fund the final blow.

US prosecutors said in December that Bankman-Fried stole billions of dollars from FTX customers to pay debts for his crypto-focused hedge fund Alameda Research, purchase lavish real estate, and donate to US political campaigns. US federal prosecutors are also investigating whether he manipulated the prices of affiliated tokens TerraUSD and Luna.

Bankman-Fried, who is out on US$250 million bail, has pleaded not guilty.

Three Arrows Capital co-founders Zhu Su (left) and Kyle Davies. PHOTOS: ZHU SU/TWITTER, KYLE DAVIES/TWITTER

Days ago, the disgraced co-founder of Temasek-backed FTX said in a blog post that he did not steal money and that Alameda failed to hedge against an “extreme” crash in the crypto markets. “I didn’t steal funds, and I certainly didn’t stash billions away,” he said.

Two of Bankman-Fried’s closest associates have pleaded guilty to defrauding the trading platform’s customers and agreed to cooperate with prosecutors’ investigation.

FTX’s venture capital backers face ‘serious questions’, US official says

Sam Bankman-Fried has been accused of stealing from FTX customers to pay debts incurred by Alameda Research. PHOTO: REUTERS

Jan 23, 2023

WASHINGTON – The failure of Sam Bankman-Fried’s FTX crypto empire raises “serious questions” about how well venture capitalists and money managers scrutinised his operations before investing client funds, a United States Commodity Futures Trading Commission (CFTC) official said.

“What kind of due diligence did they conduct?” commissioner Christy Goldsmith Romero said on Friday in a Bloomberg Television interview. “Why did they turn a blind eye to what should have been really flashing red lights?”

If a fund entrusts millions of dollars and then a year later has to write it off completely, it raises such questions, the regulator said.

She also pointed to comments by Mr John J. Ray III, who took over as FTX’s chief executive as part of its bankruptcy and has since described a lack of record-keeping and key controls when he was appointed.

It is worth considering, Ms Goldsmith Romero said, whether backers may have had potential conflicts of interest, given the interconnectedness of the crypto industry.

“Were there some conflicts that prevented them from really paying attention to the due diligence and the facts that they were uncovering?” she said.

US prosecutors meanwhile have seized nearly US$700 million (S$923 million) in assets from Bankman-Fried in January, largely in the form of Robinhood stock, according to a Friday court filing.

Bankman-Fried, who has been accused of stealing billions of dollars from FTX customers to pay debts incurred by his crypto hedge fund Alameda Research, has pleaded not guilty to fraud charges. He is scheduled to face trial in October.

The Department of Justice (DOJ) revealed the seizure of Robinhood shares earlier in January, but it provided a more complete list of seized assets on Friday, including cash held at various banks and assets deposited at crypto exchange Binance.

The ownership of the seized Robinhood shares, valued at about US$525 million, has been the subject of disputes between Bankman-Fried, FTX and bankrupt crypto lender BlockFi.

DOJ also said that assets in three Binance accounts associated with Bankman-Fried were subject to criminal forfeiture, but did not provide an estimate of the value in those accounts. BLOOMBERG, REUTERS

Is the end near for decentralised finance in 2023?

DeFi recorded muted growth last year due to the market rout, investor jitters and general financial climate. PHOTO: REUTERS

Claire Huang

Business Correspondent

Jan 30, 2023

SINGAPORE - With the crash of a series of prominent cryptocurrency exchanges last year, a lesser-understood cousin in the digital asset space – decentralised finance (DeFi) – is at a crossroads.

Observers are at odds about the fate of DeFi, with one camp believing this is the year it will shine as it turns more sustainable, while another thinks it will run out of steam because mass adoption is still out of reach.

Mr Chua U-Zyn, co-founder and chief technology officer at Singapore-based Cake DeFi, an online platform that offers access to DeFi services and products, said people are confused about what DeFi and centralised finance are.

“DeFi protocols are working really well at this time, even though in the industry, people are talking about DeFi failing. None of the major DeFi firms has even cracked a tiny bit – major ones include Uniswap and MakerDAO,” he said.

DeFi is a blockchain protocol that is governed by smart contracts. It gives users greater control over their trades.

Centralised finance (CeFi), which the bankrupt crypto exchanges are part of, gives the exchanges more control, unlike DeFi.

Of late, chatter that DeFi is failing has grown.

It comes on the back of a brutal year centralised exchanges had in 2022, when prominent players such as FTX, Celsius, Voyager and Singapore-based Hodlnaut declared bankruptcy and billions of investor monies were wiped out.

The troubles in CeFi may have pushed some investors to DeFi, but the latter recorded muted growth last year due to the market rout, investor jitters and the general financial climate.

Players point out that total decentralised exchanges (DEX) volumes across major blockchains and key protocols in DeFi have risen since the end of December, based on data from Dune.

MakerDAO, the largest DeFi loan protocol, has stayed flat since 2022, but data shows that funds have not left DeFi and that usage remains high despite falling prices, Mr Chua said.

Venture capital firm Pantera Capital, which focuses on crypto, said in its 2023 outlook note that DeFi is the future but that it needs to raise liquidity and make protocols and apps more user-friendly.

Observers said making DeFi apps and protocols easier to use will drive adoption and this will help increase liquidity in the ecosystem.

Mr Anthony Lim, a fellow for cyber security, governance and fintech at the Singapore University of Social Sciences, believes DeFi, while innovative and well intentioned, came on the scene too quickly.

He pointed out that it is understood and controlled by only a small group of players.

“The majority of the world does not really know about DeFi, let alone understand, embrace or consider it. It is more geeky than sexy.

“Then, as it moved too quickly, it started to have problems as it is not compatible with the traditional economic system the world is being run by as we know it.”

The lack of knowledge perpetuated a negative market condition in DeFi, and along with this, a loss of investor confidence and low adoption, Mr Lim said. “As long as there is a lack of mainstream adoption and critical mass, and without enough applications using it, DeFi will fade out,” he added.

But Mr Chua is bullish about DeFi’s prospects this year.

He said the days of unsustainable yields are over, and that people are more realistic and becoming more educated about how DeFi works.

“The (double-digit) yield that we’ve seen the last two years or so was mainly because of new tokens that were generated when people use DeFi products. It’s like an enticement to get into DeFi,” Mr Chua said.

Now, yields on DEXs hover at 3 per cent and 4 per cent – a sign that the returns are generated through actual use of a protocol, he said.

“So the theme for this year actually is more of a real DeFi, where the yield of DeFi is not coming from inflation or from the minting or printing of new DeFi tokens,” he added.

While only time will tell how the year will pan out for DeFi players, Mr Lim cautioned that people wanting to enter the space should think about what is in it for the various players.

Scam victim’s $10,001 used to buy Bitcoin; High Court rules crypto seller gets the money

The High Court found that there were two victims in the case - the scam victim and the man who sold his cryptocurrency. PHOTO ILLUSTRATION: REUTERS

Selina Lum

Senior Law Correspondent

JAN 30, 2023

SINGAPORE - A man who unknowingly sold his Bitcoin to a scammer was allowed to keep the money for now, even though the $10,001 used to transact the deal had come from the victim of a fraudulent bank transfer.

A High Court judge found that there were two victims in the case – the man whose stolen funds were used by the scammer to buy the Bitcoin, and the man who sold his cryptocurrency.

A court fight had ensued between the seller and the bank transfer victim after the money was seized in the course of police investigations. Each had claimed the money should be returned to him.

In a written judgment last Friday, Justice Aedit Abdullah ruled that both men had lawful possession of the money.

On the one hand, the money originated from the bank account of Mr Ling Kok Hua and was fraudulently transferred. On the other hand, Mr William Lim Tien Hou had received the money in a legitimate contractual transaction.

He ruled that the money should be returned to the individual it was seized from, which is Mr Lim.

The judge said: “I understand that both parties have been put to expense and time in dealing with the aftermath of a fraud that neither was implicated in, and which both were victims of.”

He noted that his decision was on the basis of provisions in the Criminal Procedure Code governing the return of seized property, and has no effect on a civil court if parties start a separate civil action to assert their rights.

“However, I would urge the parties to see if they can come to some sort of resolution between themselves that would avoid further time and expense for both.”

On Nov 10, 2018, a user named “haylieelan” on localbitcoins.com contacted Mr Lim – who had placed an advertisement to sell Bitcoin on the peer-to-peer trading platform – for a Bitcoin trade worth $10,000.

After Mr Lim asked “haylieelan” to provide a photograph and identity details, the user submitted a photo of Mr Ling holding his identity card and a note stating that he was buying Bitcoin from “cryptotil”, which was Mr Lim’s username.

Mr Lim received $10,000 in his bank account and released the Bitcoin to “haylieelan”. Later in the day, he received another $1 but had no idea what it was for.

On the same day, Mr Ling was duped into believing that he was communicating with his former supervisor on Facebook when, in fact, he was speaking with a scammer who had hacked the account.

Mr Ling agreed to help transfer funds to a Bitcoin trading account, which turned out to be Mr Lim’s.

Thinking that he was helping his former boss, Mr Ling provided his online banking credentials and allowed the scammer remote access to his bank account via the TeamViewer application.

Mr Ling first prepared a transfer of $1 to Mr Lim’s bank account.

At the same time, the scammer asked Mr Ling to provide a photograph showing his identity card details and a piece of paper stating that he was buying Bitcoin from “cryptotil”. Mr Ling complied.

Shortly after, the scammer asked Mr Ling to provide proof of address. He complied by taking a photograph of a letter which contained his address.

While Mr Ling was taking the two photographs, the scammer altered the sum of $1 to $10,000 and effected the transfer. Mr Ling realised this only after the transfer had gone through.

The scammer asked Mr Ling to make a further transfer of $1, and tried to alter the sum to $30,000, but Mr Ling corrected it back to $1 before effecting the transfer.

Mr Ling made a police report. Upon the conclusion of police investigations, Mr Lim and Mr Ling indicated that they would be laying competing claims on the seized money.

A disposal inquiry was held to determine how the money should be distributed.

In 2021, a district judge ruled that the sum should be returned to Mr Ling.

The district judge said Mr Lim appreciated the risks associated with Bitcoin trades, and that while he conducted due diligence checks, the money remained tainted by criminality.

Mr Lim then appealed to the High Court.

Justice Abdullah reversed the Lower Court’s decision, saying that it was immaterial whether the possession of the asset came through a risky transaction.

US charges Terra founder Do Kwon with fraud

Do Kwon was the primary developer of two cryptocurrencies whose demise roiled crypto markets around the world last year. PHOTO: BLOOMBERG

Feb 17, 2023

WASHINGTON – The US Securities and Exchange Commission (SEC) has charged crypto developer Do Kwon and his company Terraform Labs with defrauding investors in what the regulator deemed a multibillion-dollar scheme, according to a filing in federal court.

Kwon founded blockchain platform Terraform Labs and was the primary developer of two cryptocurrencies whose demise roiled crypto markets around the world last year. He raised billions of dollars from investors beginning in April 2018 by selling a series of interconnected digital assets, many of which were unregistered securities, the SEC alleged in the court filing in the Southern District of New York.

The SEC filing did not say where Kwon was living. In September, a South Korean court issued an arrest warrant alleging that Kwon was residing in Singapore, but the Singapore Police Force said he was not currently in the city-state. Kwon could not immediately be reached for comment.

TerraUSD, an algorithmic stablecoin supposed to maintain a 1:1 peg to the United States dollar, derived its value through another paired token called Luna.

Both tokens lost nearly all their value when TerraUSD, also known as UST, slipped below its 1:1 dollar peg in May 2022. Prior to its collapse on May 9, TerraUSD had a market cap of more than US$18.5 billion (S$24.7 billion) and was the 10th-largest cryptocurrency.

According to the SEC’s complaint, Terraform Labs and Kwon misled investors about the stability of TerraUSD, and claimed that the firm’s crypto tokens would increase in value.

Terraform Labs did not immediately respond to a request for comment.

“This case demonstrates the lengths to which some crypto firms will go to avoid complying with the securities laws, but it also demonstrates the strength and commitment of the SEC’s dedicated public servants,” said SEC chair Gary Gensler in a statement.

Globally, investors in TerraUSD and Luna lost an estimated US$42 billion, according to blockchain analytics firm Elliptic.

The market turmoil that ensued after the collapse of TerraUSD led to the failure of several major crypto companies, including US crypto lender Celsius Network and Singapore-based crypto fund manager Three Arrows Capital. REUTERS

‘Whales’ profited at the expense of retail investors in 2022 crypto crash, BIS study finds

Large investors were able to sell their crypto assets to smaller ones before prices collapsed, said the BIS researchers. PHOTO: REUTERS

Feb 22, 2023

NEW YORK - When the Terra ecosystem collapsed in 2022 and again as FTX fell apart, retail investors rushed to buy the big crypto dip. Meanwhile, “whales” were selling en masse – all at the expense of those smaller mom-and-pop traders.

This is according to a study by the influential Bank for International Settlements (BIS).

After analysing crypto exchange data, it concluded that many at-home investors lost money on their investments – likely exacerbated by larger, or more sophisticated, players selling their coins right before the steep price declines seen in 2022.

Owners of large wallets – which the report calls “whales” – reduced their holdings of Bitcoin in the days after the “shock episodes”.

Medium-sized investors and smaller ones – referred to as “krill” – increased their exposures.

“The price patterns suggest that larger investors were able to sell their assets to smaller ones before the steep price decline,” said the BIS researchers. “Large holders thus profited at the expense of smaller investors.”

“In stormy seas, ‘the whales eat the krill,’” wrote economists Giulio Cornelli, Sebastian Doerr, Jon Frost and Leonardo Gambacorta in a report dated Feb 20. “Retail investors have chased prices, and most have lost money.”

The trend is just the latest evidence that the industry needs greater investor protection, said the report.

Last year tested the resolve of all types of investors, with the calamitous crash of previously well-regarded projects, including Terra/Luna and FTX.

Bitcoin fell more than 64 per cent in 2022, starting the year at around US$47,300 and closing it at near US$16,500, according to data compiled by Bloomberg.

Digital-asset investors have their own terms for those who hold – or “hodl” – through even the roughest of times. The term “hodl” means “hold on for dear life”. Investors who suffer through steep losses and hold on even as they watch their investments continually lose value are sometimes referred to as “bag holders”.

To investigate crypto-trading patterns, BIS researchers built a database of retail investor use of exchange apps across 95 countries, with data spanning between August 2015 and December 2022.

The team found that as prices rose in that stretch – with Bitcoin reaching a near US$69,000 high in November 2021 – more and more users entered the system. The monthly average number of daily active users ballooned to more than 30 million worldwide from 100,000, they said.

The study makes some big assumptions. For example, researchers found that three-quarters of users who downloaded exchange apps were using them when Bitcoin was above US$20,000. They assumed that each new user bought US$100 of Bitcoin in the first month of their app download and in each subsequent month.

But the fact that adoption rises as prices are increasing suggests that many users were wading in simply because they were attracted by high prices and oftentimes expected prices to continue to go up, the BIS said.

Yet over the course of 2022, amid the downfall of Terra/Luna, as well as the swift disintegration of FTX, crypto tokens suffered big losses. Trading activity, meanwhile, picked up “markedly”.

“These patterns suggest that users tried to weather the storm by adjusting their portfolios away from owning tokens under stress towards other crypto assets, including asset-backed stablecoins,” the BIS wrote. BLOOMBERG

IMF lays out crypto action plan, recommends against legal tender status

The International Monetary Fund's top recommendation was not to grant crypto assets official currency or legal tender status. PHOTO: REUTERS

Feb 24, 2023

LONDON – The International Monetary Fund (IMF) has laid out a nine-point action plan for how countries should treat crypto assets, with point No. 1 a plea not to give cryptocurrencies such as Bitcoin legal tender status.

The global lender of last resort said its executive board had discussed a paper, Elements Of Effective Policies For Crypto Assets, that provided “guidance to IMF member countries on key elements of an appropriate policy response to crypto assets”.

Such efforts have become a priority for the authorities, the fund said, after the collapse of a number of crypto exchanges and assets over the last couple of years, adding that doing nothing was now “untenable”.

The top recommendation was “safeguard monetary sovereignty and stability by strengthening monetary policy frameworks and do not grant crypto assets official currency or legal tender status”.

The IMF had hit out at El Salvador in late 2021 when the Central American country became the first to adopt Bitcoin as legal tender, a move that has since been copied by the Central African Republic.

Other advice on Thursday’s list, which comes as Group of 20 decision-makers meet in India, included guarding against excessive capital flows, adopting unambiguous tax rules and laws around crypto assets, and developing and enforcing oversight requirements for all crypto market actors.

Countries should also establish international arrangements to enhance supervision and enforce regulations, the IMF added, as well as set up ways to monitor crypto’s impact on the stability of the global monetary system.

Outlining its executive board’s assessment, the IMF said the directors welcomed the proposals and agreed that the widespread adoption of crypto assets “could undermine the effectiveness of monetary policy, circumvent capital flow management measures, and exacerbate fiscal risks”.

It added that they also “generally agreed” that crypto assets should not be granted official currency or legal tender status, and though strict bans of assets are “not the first-best option”, a few directors thought these should not be ruled out. REUTERS

Temasek, other institutions sued for ‘aiding and abetting’ FTX fraud

Eighteen defendants were named in a class action lawsuit filed by one of FTX's customers, with Temasek being one of them. PHOTO: REUTERS

Aqil Hamzah

Feb 24, 2023

SINGAPORE – Investment company Temasek was named in a class action lawsuit filed in Miami, Florida, on Wednesday as one of 18 defendants that allegedly conspired with troubled cryptocurrency exchange FTX to defraud customers.

The complaint was filed by one of the exchange’s customers, Mr Connor O’Keefe, a Mississippi resident, on behalf of himself and “all others similarly situated”.

The suit claimed that “defendant venture capital firms wielded their power, influence and deep pockets to launch FTX’s house of cards to its multi-billion dollar scale”. The class members are seeking compensatory and punitive damages, among other reliefs.

These firms named include the New York-based Signature Bank, as well as venture capital firms such as Sequoia Capital Operations and Softbank Vision Fund.

The 83-page document seen by The Straits Times alleges that the firms had been aware of fraud being committed by FTX, by virtue of conducting due diligence checks prior to their investments.

It cited a Nov 17, 2022, statement on Temasek’s website days after FTX filed for bankruptcy protection in the US, which said: “We conducted an extensive due diligence process on FTX, which took approximately eight months from February to October 2021.”

This included looking into the associated regulatory risk with crypto financial market service providers, as well as combing through the exchange’s audited financial statement.

As part of its process, Temasek had also sought the advice of external legal and cybersecurity specialists, and interviewed people familiar with the company, namely employees, industry participants and other investors.

The statement said: “Throughout the multiple rounds of due diligence, FTX demonstrated a clear willingness to discuss and engage with us, which indicated that they were willing to do business in the right way.

“During this process, we enquired about the relationship, preferential treatment, and separation between Alameda and FTX, and were given appropriate confirmations that were contractually binding.”

It reiterated that its US$275 million (S$369.7 million) investment into FTX was not made into cryptocurrencies, with its US$210 million investment for a minority stake of about 1 per cent in Bahamas-headquartered FTX International, while the other US$65 million was for a minority stake of about 1.5 per cent in FTX US, the American subsidiary.

Sam Bankman-Fried, the firm’s embattled co-founder and former chief executive of the once-prominent cryptocurrency exchange, has been accused of stealing billions of dollars from customers to plug losses incurred by sister firm Alameda Research, which acted as his hedge fund.

In response to queries from ST, a Temasek spokesman said it was aware of the lawsuit, but declined to comment as it is an ongoing legal matter.

The Wall Street Journal quoted a spokesman for Signature Bank as saying the allegations had no merit, while Softbank declined to comment.

The United States Securities and Exchange Commission (SEC) in December 2022 charged Bankman-Fried with defrauding FTX investors, and on Thursday, he was handed four new criminal charges in a New York federal court.

The latest 12-count indictment accuses him of concealing “the fact that Alameda had taken billions of dollars from FTX” from the hedge fund’s lenders and FTX’s equity investors.

Bankman-Fried, who is currently out on a US$250 million bond, is set to face trial on Oct 2.

US watchdog warns of risks of buying crypto asset securities

The SEC has been cracking down on the crypto industry, which its chair has called a “Wild West” riddled with misconduct. PHOTO: REUTERS

Mar 24, 2023

NEW YORK - The United States Securities and Exchange Commission (SEC) on Thursday issued an investor alert warning that firms offering crypto asset securities may not be complying with US laws.