- Joined

- May 25, 2011

- Messages

- 996

- Points

- 28

http://www.smh.com.au/business/prop...officially-over-ubs-says-20171101-gzclp4.html

Australia's world record housing boom is 'officially' over, UBS says

"There is now a persistent and sharp slowdown unfolding", ending 55 years of unprecedented growth that has seen home values soar by more than 6500 per cent, UBS economists wrote in a note to clients on Thursday.

Australian census property snapshot

A brief look at how property tenure has changed over the last 25 years.

Home prices in the capital cities have continued to slow on a quarterly basis, weighed down by tighter lending requirements for property investors and banks' out-of-cycle raising of home loan rates.

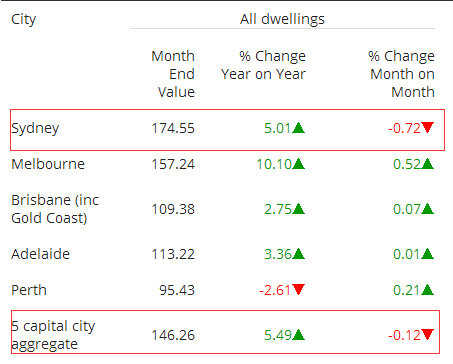

In Sydney, home prices fell 0.6 per cent over the quarter and were down 0.5 per cent over the month, figures from property data group Corelogic showed on Thursday morning.

Related Articles

Nationally, home prices stayed flat over the month and edged up only 0.4 per cent over the three months to October 31.

UBS had previously been cautious on the market, forecasting Australia's annual home price growth would moderate from solid double digits to 7 per cent in 2017, before prices would even fall by 0.3 per cent in 2018.

Business AM Newsletter

Get the latest news and updates emailed straight to your inbox.

By submitting your email you are agreeing to Fairfax Media's terms and conditions and privacy policy.

But the recent weakness in auction clearance rates and anaemic price growth over the past five months suggested "the cooling may be happening a bit more quickly than even we expected", economists George Tharenou and Carlos Cacho wrote in their note, downgrading their growth forecast for 2017 to just 5 per cent.

Home prices in Sydney have fallen for the second month in a row. Photo: Supplied

The cooling house prices and a slowdown in demand for loans to property investors suggested a "tightening of financial conditions", which will likely weigh on consumer spending and prompt the Reserve Bank to keep interest rates on hold until the second half of next year, they added.

Despite the recent downturn in values, Sydney home prices are up 74 per cent since the latest growth cycle began in early 2012

Going, going, gone: Australia's housing boom is "offically" over, UBS says.

However, the latest figures show it may now be more lucrative investing on the sharemarket than in property, CommSec's chief economist Craig James suggested in a separate note.

Total returns on shares rose by 15.5 per cent in the year to October while total returns on capital city homes rose by 10.7 per cent, he pointed out.

With a record amount of new property supply such as new apartments and townhouses coming onto the market, and stalling wages and rising energy prices sapping consumers' chances of saving up money for home deposits, property price growth is unlikely to bounce back in the near future, according to Commonwealth Bank's senior economist, John Peters.

"It is hard to see this situation reversing anytime soon with consumers now running down their savings to maintain current living standards and paying bills," he warned.

With AAP

Related Articles

Australia's world record housing boom is 'officially' over, UBS says

- Miriam Steffens

- facebook SHARE

- twitter TWEET

"There is now a persistent and sharp slowdown unfolding", ending 55 years of unprecedented growth that has seen home values soar by more than 6500 per cent, UBS economists wrote in a note to clients on Thursday.

Australian census property snapshot

A brief look at how property tenure has changed over the last 25 years.

Home prices in the capital cities have continued to slow on a quarterly basis, weighed down by tighter lending requirements for property investors and banks' out-of-cycle raising of home loan rates.

In Sydney, home prices fell 0.6 per cent over the quarter and were down 0.5 per cent over the month, figures from property data group Corelogic showed on Thursday morning.

Related Articles

- The suburbs where one in every four houses sells for under $650,000

- 'Significant turn of events': Sydney property prices raise alarm

Nationally, home prices stayed flat over the month and edged up only 0.4 per cent over the three months to October 31.

UBS had previously been cautious on the market, forecasting Australia's annual home price growth would moderate from solid double digits to 7 per cent in 2017, before prices would even fall by 0.3 per cent in 2018.

Business AM Newsletter

Get the latest news and updates emailed straight to your inbox.

By submitting your email you are agreeing to Fairfax Media's terms and conditions and privacy policy.

But the recent weakness in auction clearance rates and anaemic price growth over the past five months suggested "the cooling may be happening a bit more quickly than even we expected", economists George Tharenou and Carlos Cacho wrote in their note, downgrading their growth forecast for 2017 to just 5 per cent.

- Share on Facebook SHARE

- Share on Twitter TWEET

Home prices in Sydney have fallen for the second month in a row. Photo: Supplied

The cooling house prices and a slowdown in demand for loans to property investors suggested a "tightening of financial conditions", which will likely weigh on consumer spending and prompt the Reserve Bank to keep interest rates on hold until the second half of next year, they added.

Despite the recent downturn in values, Sydney home prices are up 74 per cent since the latest growth cycle began in early 2012

- Share on Facebook SHARE

- Share on Twitter TWEET

Going, going, gone: Australia's housing boom is "offically" over, UBS says.

However, the latest figures show it may now be more lucrative investing on the sharemarket than in property, CommSec's chief economist Craig James suggested in a separate note.

Total returns on shares rose by 15.5 per cent in the year to October while total returns on capital city homes rose by 10.7 per cent, he pointed out.

With a record amount of new property supply such as new apartments and townhouses coming onto the market, and stalling wages and rising energy prices sapping consumers' chances of saving up money for home deposits, property price growth is unlikely to bounce back in the near future, according to Commonwealth Bank's senior economist, John Peters.

"It is hard to see this situation reversing anytime soon with consumers now running down their savings to maintain current living standards and paying bills," he warned.

With AAP

Related Articles