The only job they do also screw up.

-

IP addresses are NOT logged in this forum so there's no point asking. Please note that this forum is full of homophobes, racists, lunatics, schizophrenics & absolute nut jobs with a smattering of geniuses, Chinese chauvinists, Moderate Muslims and last but not least a couple of "know-it-alls" constantly sprouting their dubious wisdom. If you believe that content generated by unsavory characters might cause you offense PLEASE LEAVE NOW! Sammyboy Admin and Staff are not responsible for your hurt feelings should you choose to read any of the content here. The OTHER forum is HERE so please stop asking.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Investments gone bad

- Thread starter LITTLEREDDOT

- Start date

So that can huat big big mah...The only job they do also screw up.

head u lost, tail u also lost,kym?

Sats says it ‘remains on track to restoring profitability’ after 3 straight years of losses

Sats reiterated that there is no risk of it being placed on SGX's watch list. PHOTO: ST FILE

Dec 5, 2023

SINGAPORE – In-flight caterer and ground handler Sats on Dec 5 said it remains on track to restore profitability, a week after it filed its notice of three consecutive years of losses.

The group was responding to media articles detailing the notice, its US$3 billion (S$4 billion) multi-currency debt issuance programme and the uncommitted bilateral facilities it has obtained.

In its clarification, Sats said its financial performance reported over the past three years reflects the unprecedented impact of Covid-19 on the group’s business.

The company wished to assure investors that it remains on track to restoring profitability on the back of global travel recovery, new contract wins, operational efficiencies and synergies achieved through the integration with Worldwide Flight Services (WFS).

It reiterated that there is no risk of it being placed on the Singapore Exchange (SGX) watch list, as its six-month average daily market capitalisation stood at $3.9 billion.

Based on SGX listing rules, mainboard-listed companies will be placed on the watch list if they record pre-tax losses for the three latest consecutive financial years and fail to maintain an average daily market cap of at least $40 million over the last six months.

As for its funding programmes, the group said its $3 billion multi-currency debt issuance programme will provide flexibility for the group to access global debt markets to optimise its borrowing costs through appropriate maturity tenure.

It noted that it continues to generate positive net operating cash flow on the back of the global travel recovery and good progress on its integration with WFS.

Its newly obtained uncommitted bilateral facilities were also the result of the group restructuring WFS’ existing revolving credit facilities, which had certain restrictive covenants in place.

Sats had restructured these facilities with ING Bank, MUFG Bank, Bank of America and HSBC to remove these restrictive covenants and provide the group with greater funding flexibility, the group said.

The group said it will continue to maintain a prudent financial management strategy, as well as focus on delivering stable financial performance and increasing shareholder value.

Sats shares were trading up two cents, or 0.8 per cent, to $2.68 as at 9.35am on Dec 5 after its latest statement. THE BUSINESS TIMES

No worry, many high ses rich tiong comingSats says it ‘remains on track to restoring profitability’ after 3 straight years of losses

Sats reiterated that there is no risk of it being placed on SGX's watch list. PHOTO: ST FILE

Dec 5, 2023

SINGAPORE – In-flight caterer and ground handler Sats on Dec 5 said it remains on track to restore profitability, a week after it filed its notice of three consecutive years of losses.

The group was responding to media articles detailing the notice, its US$3 billion (S$4 billion) multi-currency debt issuance programme and the uncommitted bilateral facilities it has obtained.

In its clarification, Sats said its financial performance reported over the past three years reflects the unprecedented impact of Covid-19 on the group’s business.

The company wished to assure investors that it remains on track to restoring profitability on the back of global travel recovery, new contract wins, operational efficiencies and synergies achieved through the integration with Worldwide Flight Services (WFS).

It reiterated that there is no risk of it being placed on the Singapore Exchange (SGX) watch list, as its six-month average daily market capitalisation stood at $3.9 billion.

Based on SGX listing rules, mainboard-listed companies will be placed on the watch list if they record pre-tax losses for the three latest consecutive financial years and fail to maintain an average daily market cap of at least $40 million over the last six months.

As for its funding programmes, the group said its $3 billion multi-currency debt issuance programme will provide flexibility for the group to access global debt markets to optimise its borrowing costs through appropriate maturity tenure.

It noted that it continues to generate positive net operating cash flow on the back of the global travel recovery and good progress on its integration with WFS.

Its newly obtained uncommitted bilateral facilities were also the result of the group restructuring WFS’ existing revolving credit facilities, which had certain restrictive covenants in place.

Sats had restructured these facilities with ING Bank, MUFG Bank, Bank of America and HSBC to remove these restrictive covenants and provide the group with greater funding flexibility, the group said.

The group said it will continue to maintain a prudent financial management strategy, as well as focus on delivering stable financial performance and increasing shareholder value.

Sats shares were trading up two cents, or 0.8 per cent, to $2.68 as at 9.35am on Dec 5 after its latest statement. THE BUSINESS TIMES

SGX-listed Spac Pegasus Asia will not conclude business combination, and dissolve

Singapore-listed Spacs have until January 2024 to announce their potential business combination, which is also known as a de-Spac transaction. PHOTO: BT FILE

Kang Wan Chern

Deputy Business Editor

Dec 20, 2023

SINGAPORE – Adverse market conditions have deterred the special purpose acquisition company (Spac) Pegasus Asia from concluding a combination with another business.

The Singapore Exchange (SGX)-listed firm will tell shareholders at a later date how they can redeem their stock.

The Spac will then cease operations and wind up its business. There will be no redemption rights nor liquidating distributions regarding its warrants.

Spacs are designed to acquire another company and raise money through an initial public offering (IPO) within two years of their own IPO, a process known as a de-Spac transaction.

If the Spac cannot find a suitable acquisition target, it must dissolve and return the funds to investors, a fate that has befallen Pegasus.

Despite the disappointing outcome, a Singapore Exchange spokesman noted that “the Spac framework is here to stay in the long term and complements the traditional IPO route”.

“The framework was launched to offer listing aspirants greater certainty on price and execution. New structures and products such as Spacs offer wider choices to both issuers and investors.”

Pegasus, which raised gross proceeds of $170 million in its January 2022 IPO, is sponsored by European asset manager Tikehau Capital and Financiere Agache, a luxury goods company backed by LVMH chief executive Bernard Arnault’s family office.

The three Spacs listed here have not enjoyed a good start, marked by the “disastrous de-Spac involving 17Live”, as accounting professor Mak Yuen Teen from the NUS Business School put it.

Vertex Technology Acquisition Corporation (VTAC), a Spac backed by Vertex Venture Holdings and a subsidiary of Singapore’s investment company Temasek, merged with livestreaming platform 17Live on Dec 8.

VTAC shareholders redeemed about 62.53 per cent of the Spac’s share capital after several analysts concluded ahead of the merger that its shares were overvalued.

17Live shares have plunged following the business combination, closing at $1.55 on Dec 20, down 65.78 per cent from VTAC’s IPO price of $5.

The third and remaining SGX-listed Spac, Novo Tellus Alpha Acquisition (NTAA), has until January 2024 to announce a potential business combination.

NTAA shares closed up 2 per cent at $5 on Dec 20 while Pegasus stock closed up 2.7 per cent at $4.97.

Securities Investors Association (Singapore) president David Gerald noted that Pegasus’ decision to liquidate is “a much better outcome than it rushing into a badly structured business combination at a lofty valuation”.

He added that the SGX could fine-tune the Spac structure based on the experience of the first three Spacs, noting: “There is nothing fundamentally wrong with the Spac and this outcome had more to do with market conditions.

“Notably, interest rates have risen sharply. Such considerations may have impacted the sponsor’s decision in liquidating the Spac, as it may be harder to find attractive targets and investors’ appetite for growth assets are now lower.”

Prof Mak noted that good companies usually opt to list via IPOs, while those looking to list through a Spac are likely to prefer the US market for liquidity and valuation.

Mr Nirgunan Tiruchelvam, head of consumer and Internet at investment firm Aletheia Capital, said the hype over Singapore Spacs has simmered now that the market environment is once again better suited for IPOs with the United States Federal Reserve considering rate cuts in the year ahead.

He added that Pegasus would have been afraid of not being able to find a well-valued target and worried that a de-Spac would go the way of 17Live.

“Retail investors would also be asking what’s the whole point of raising funds through a Spac, which involves high fees, just for it to get into a shotgun marriage that might not last for the long term.”

Singapore-listed Spacs have until January 2024 to announce their potential business combination, which is also known as a de-Spac transaction. PHOTO: BT FILE

Kang Wan Chern

Deputy Business Editor

Dec 20, 2023

SINGAPORE – Adverse market conditions have deterred the special purpose acquisition company (Spac) Pegasus Asia from concluding a combination with another business.

The Singapore Exchange (SGX)-listed firm will tell shareholders at a later date how they can redeem their stock.

The Spac will then cease operations and wind up its business. There will be no redemption rights nor liquidating distributions regarding its warrants.

Spacs are designed to acquire another company and raise money through an initial public offering (IPO) within two years of their own IPO, a process known as a de-Spac transaction.

If the Spac cannot find a suitable acquisition target, it must dissolve and return the funds to investors, a fate that has befallen Pegasus.

Despite the disappointing outcome, a Singapore Exchange spokesman noted that “the Spac framework is here to stay in the long term and complements the traditional IPO route”.

“The framework was launched to offer listing aspirants greater certainty on price and execution. New structures and products such as Spacs offer wider choices to both issuers and investors.”

Pegasus, which raised gross proceeds of $170 million in its January 2022 IPO, is sponsored by European asset manager Tikehau Capital and Financiere Agache, a luxury goods company backed by LVMH chief executive Bernard Arnault’s family office.

The three Spacs listed here have not enjoyed a good start, marked by the “disastrous de-Spac involving 17Live”, as accounting professor Mak Yuen Teen from the NUS Business School put it.

Vertex Technology Acquisition Corporation (VTAC), a Spac backed by Vertex Venture Holdings and a subsidiary of Singapore’s investment company Temasek, merged with livestreaming platform 17Live on Dec 8.

VTAC shareholders redeemed about 62.53 per cent of the Spac’s share capital after several analysts concluded ahead of the merger that its shares were overvalued.

17Live shares have plunged following the business combination, closing at $1.55 on Dec 20, down 65.78 per cent from VTAC’s IPO price of $5.

The third and remaining SGX-listed Spac, Novo Tellus Alpha Acquisition (NTAA), has until January 2024 to announce a potential business combination.

NTAA shares closed up 2 per cent at $5 on Dec 20 while Pegasus stock closed up 2.7 per cent at $4.97.

Securities Investors Association (Singapore) president David Gerald noted that Pegasus’ decision to liquidate is “a much better outcome than it rushing into a badly structured business combination at a lofty valuation”.

He added that the SGX could fine-tune the Spac structure based on the experience of the first three Spacs, noting: “There is nothing fundamentally wrong with the Spac and this outcome had more to do with market conditions.

“Notably, interest rates have risen sharply. Such considerations may have impacted the sponsor’s decision in liquidating the Spac, as it may be harder to find attractive targets and investors’ appetite for growth assets are now lower.”

Prof Mak noted that good companies usually opt to list via IPOs, while those looking to list through a Spac are likely to prefer the US market for liquidity and valuation.

Mr Nirgunan Tiruchelvam, head of consumer and Internet at investment firm Aletheia Capital, said the hype over Singapore Spacs has simmered now that the market environment is once again better suited for IPOs with the United States Federal Reserve considering rate cuts in the year ahead.

He added that Pegasus would have been afraid of not being able to find a well-valued target and worried that a de-Spac would go the way of 17Live.

“Retail investors would also be asking what’s the whole point of raising funds through a Spac, which involves high fees, just for it to get into a shotgun marriage that might not last for the long term.”

Two remaining SGX-listed spac firms to dissolve, ending further despac hopes

Khairani Afifi Noordin

Wed, Dec 20, 2023

")

Should the spacs be dissolved, investors’ funds will be returned. Photo: Albert Chua/The Edge Singapore

Singapore Exchange (SGX)-listed spac firms Pegasus Asia and Novo Tellus Alpha Acquisition (NTAA) are not looking to merge with any target companies and are instead seeking to dissolve the blank-cheque companies, according to sources familiar with the matter.

This is on the back of lower-than-expected numbers owing to unfavourable market conditions, The Edge Singapore understands. Pegasus’ announcement is expected to be made by Dec 22 while NTAA’s is set to be released next week. The deadline for SGX-listed despac mergers is January 2024.

Should the spacs be dissolved, investors’ funds will be returned. The Edge Singapore has reached out to both Pegasus and NTAA to seek clarification.

In September, The Edge Singapore reported that Pegasus was targeting Singapore-based Kacific Satellites.

Founded by Christian Patourax in 2013, Kacific operates wholesale broadband satellite services, serving telecom operators, ISPs and governments. It boasts experienced global telecom and infrastructure investors.

Kacific launched its first Ka-band high throughput satellite, Kacific-1, in 2019 to stream high-speed, low-cost and ultra-reliable broadband to rural and suburban areas of the Pacific and Southeast Asia. One of the company’s longtime partners is ST Engineering iDirect, the satellite innovation arm of SGX-listed ST Engineering, which provides Kacific with ground infrastructure.

Learn More

Meanwhile, in a response to The Edge Singapore's report via a filing dated Dec 20, NTAA executive chairman and CEO Loke Wai San says the company has not identified a conclusive target and will make the relevant disclosures at the appropriate time.

Under SGX's rules, the despacs are to take place within two years, although an extension of a year can be given, subject to approvals. As NTAA commenced trading on Jan 27 2022, it is likely that the spac would need to apply for the aforementioned extension.

The only SGX-listed spac that has successfully completed a business combination is Vertex Technology Acquisition Corp (VTAC), having merged with live-streaming platform 17LIVE following an EGM on Dec 1. Notably, institutional investors such as Fullerton Fund Management and NTUC Income have fully redeemed their shares.

On the day of the EGM, VTAC announced that 62.53% of the company's issued share capital have been redeemed as at Nov 29.

Shares in 17LIVE closed at $1.56 on Dec 19, almost 70% lower than VTAC’s IPO price of $5.

GIC among funds that bought Signa’s equity-like securities

According to an insolvency filing from Signa Prime Selection, GIC owns €85 million of profit participation securities known as genussrechte or genussscheine. PHOTO: GIC

Jan 8, 2023

LONDON – Saudi Arabia’s Public Investment Fund (PIF) and Singapore’s GIC are among the investors listed as holders of riskier equity-like instruments issued by Signa’s luxury real estate unit, now caught up in insolvency proceedings in Austria.

PIF owns €287 million (S$417.6 million) of the profit participation securities, known as genussrechte or genussscheine, while the Singapore sovereign wealth fund owns €85 million, according to the insolvency filing from Signa Prime Selection, dated Dec 28, seen by Bloomberg News.

Profit participation rights are subordinated securities that grant holders a share of the issuer’s profits. Bloomberg News previously reported that PIF had exposure to the ailing Austrian real estate group’s junior debt.

Representatives of PIF and GIC declined to comment. A spokesperson for Signa did not respond to a request for comment.

How much these investors will be able to recoup from these investments during the insolvency process remains unclear.

The two main property units of Austrian retail and real estate entrepreneur Rene Benko’s Signa group, Signa Prime and Signa Development Selection, filed for court-supervised self-administration proceedings in December.

Signa Prime and Signa Development are looking to raise €350 million in total via new profit participation securities as part of their insolvency plan, according to filings seen by Bloomberg News.

Unlike the existing profit participation rights, the new funding would not be part of the claims treated under Signa’s restructuring arrangement, but would rather help fund it.

Close ties

The insolvency filings highlight how Mr Benko was able to tap deep-pocketed and far-flung investors through a variety of financing.Take for example Signa’s Bahnhofplatz 7 project in Munich, which was to renovate the Hermann Tietz department store and construct the new Corbinian office building. Signa Prime guaranteed €117 million of financing from PIF to the firm that ran the development, according to the insolvency filing. Corporate filings show how PIF bought €187 million of profit participation certificates linked to that project, guaranteed by Signa Prime, back in March 2022.

PIF is not the only Middle East investor listed. The insolvency filing also shows €93 million in guaranteed financing from Sign Holdings RSC, a special purpose vehicle registered in Abu Dhabi.

AC, a prominent Dubai investment fund, is shown as linked to the vehicle in the insolvency filing. About a third of funding went to the five-star Bauer Hotel in Venice. A spokesperson for AC did not immediately respond to requests for comment.

The insolvency filing also discloses a €200 million corporate loan granted by a company with directors from Germany’s Schoeller Group, founded by the industrial family of that name. The financing was granted to Signa Prime Capital Invest, a subsidiary of Signa Prime Selection, according to the filing.

Signa Prime’s and Signa Development’s insolvency filings did not give a comprehensive breakdown of total exposure, meaning that specific creditors could have larger holdings than indicated.

New funds

Whether existing investors will be tempted to plough fresh cash into the business to protect their positions is still an open question. If secured, the fresh financing will allow the Signa units to remain in an insolvency proceeding known as self-administration, where management remains in place.Signa Prime is seeking at least €300 million, while Signa Development is seeking €50 million, according to the insolvency filings.

Signa Development is offering to issue profit participation certificates at an interest rate of 9 per cent, as stated in a separate document seen by Bloomberg. The unit is looking to issue them as soon as January, and they will mature in December 2025, although it may have extension options.

On top of paying out interest, 33 per cent of the liquidity surplus at the end of 2024 will also be allocated to the holders of these instruments. There is a maximum cap, though, set at 70 per cent of the profit participation rights’ nominal amount. The instruments come with no collateral, according to the document.

In an interview on Jan 5 with German business newspaper Handelsblatt, Austrian construction magnate Hans Peter Haselsteiner – who is a shareholder in Signa Holding and Development – said he can “picture” signing participation rights to provide new cash and support the firm’s insolvency proceedings. BLOOMBERG

How Singapore’s Regulators have failed Noble’s Investors and Shielded the Fraudsters

August 29, 2022The Monetary Authority of Singapore (“MAS”) has imposed a civil penalty of SG$12.6m (equivalent to US$9m) on Noble Group, more than seven years after Iceberg exposed the fraud. The regulators have discovered that long term commodity contracts were inflated, something that everyone already knew.

This fine represents just:

- 2.7% of the total remuneration of Noble’s directors from 2008-2017. Most of this figure went to the pockets of Noble founder Richard Elman and its former CEO, Will Randall.

- 10.7 % of what auditor E&Y earned from Noble over the same period

- 0.15% of the market cap lost since February 2015, when Iceberg first published on Noble.

The fine will be paid on a “voluntary basis”, whatever that means. The Public Accountants Oversight Committee (PAOC) also ordered NRI auditor E&Y to “attend specific courses”. The Accounting and Corporate Regulatory Authority (ACRA) issued “stern warnings” to two former directors. That sounds scary. However, they refused to reveal their names because… it could hurt their feelings?

Here is the list of NRI directors in 2016:

- Jeffrey Alam

- Neil Dhar

- Will Randall

- Jeff Frase

- Paul Jackaman

- Tim Eyre

Thousands of individual investors are left high and dry. Their life savings, invested in this once-upon-a-time blue chip, will never be seen again. Unfortunately, my friends, individual investors like you do not count in Singapore. Your hard-earned money has been used to fund the bank accounts and lavish lifestyles of Noble’s managers.

Stock exchange regulators are defined by the actions they take against major frauds. Noble’s fraudsters will get away with no consequence in Singapore. I compared Noble to Enron in my reports because of the similarities in their accounting practices, and both filed for bankruptcy. But the regulatory environment made all the difference. Enron’s management faced a jury after nine months. Its CEO and CFO served time in prison. Singapore regulators, on the other hand, took seven years for a slap on the wrist and some “stern” warnings.

The outcome is unsurprising as the tone was set as far back as 2015 when I had conference calls with MAS and SGX (the stock exchange) representatives. I was introduced to them by Michael Dee, former CEO of Morgan Stanley South Asia, ex-Temasek MD, and another critic of Noble. My expectations were low because of a bad experience with the Maritime Port Authority, another regulator in Singapore.

Anyway, I still spoke to the MAS and SGX. Nobody could blame me for not trying.

The discussions were unimpressive. My interlocutors showed little enthusiasm for digging into the nitty-gritty. I tried to explain that two days was all they needed to get specific information to know with absolute certainty if the books were cooked. They didn’t seem interested.

In June 2016. Noble was allowed to raise more capital even though the evidence of cooked accounts was piling up. Many retail investors saw this as a positive signal. Sophisticated investors sat on the sidelines. The regulators were truly irresponsible: retail investor losses deepened while Noble’s managers continued to pay themselves nice salaries.

After I published my reports, Noble retaliated against me. I was under 24/7 surveillance. Investigators followed me around. I received physical threats that I knew came from Noble. There were constant attempts to hack my computer. I filed a complaint with the Hong Kong police. Noble was then issued with a police warning, as there was enough evidence against them. The lawsuit was also draining my financial resources. Noble’s goal was to bankrupt me. My financial resources were limited as Iceberg Research had not started its activity as a short seller. I reported the harassment to the regulators in the hopes of sending a strong message to Noble. They told me it was not their problem. Perhaps they have never heard of whistleblower protection?

Singapore has a unique regulatory environment. The frontline regulator is SGX’s own subsidiary: SGX RegCo, run by Mr. Tan Boon Gin.

Head of SGX RegCo Tan Boon Gin

The SEC in contrast is an independent agency that oversees securities markets in the US. The SGX’s priority was never to go after fraudsters. Noble was an index constituent with substantial trading volumes. This was what mattered: protect the money flow. The SGX would insist that RegCo is an independent entity. I don’t know about that. Would you incorporate a subsidiary if you want the company to be independent? Mr. Tan also received a total remuneration of US$1.2m in 2021, which is a very nice salary, even by Singapore’s standards. He earned a total of US$4.1m between 2018 and 2021. I doubt SGX would pay Mr. Tan so much if he started to rock the boat. Meanwhile, frauds and scandals pile up on this small stock exchange: Best World, Hyflux, Eagle Hospitality… Enforcement is virtually non-existent.

Some voices in Singapore may argue that the “light touch” regulatory approach is essential: business would be hampered by too much regulation. This argument is easily refuted.

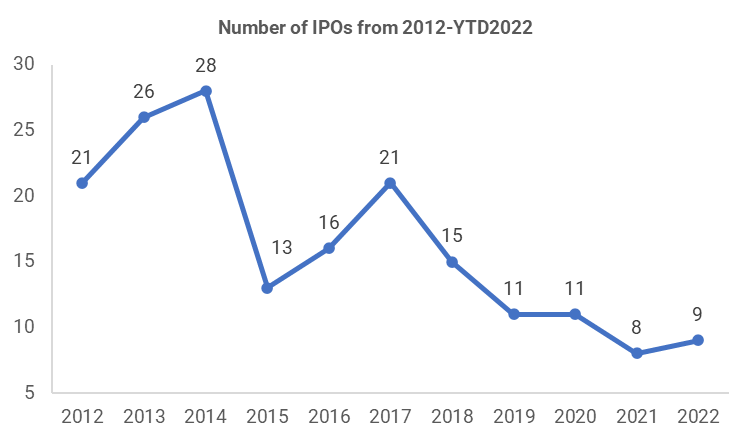

Historically, SGX was able to attract high-quality companies from around South Asia, expanding its market beyond its own country. But the number of new listings has declined over the years.

Source: SGX Website

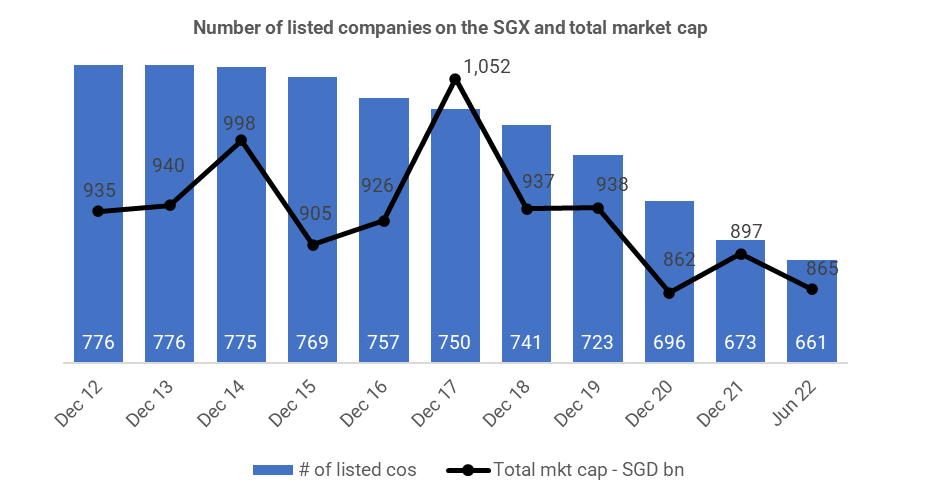

And along with delistings, the number of listed companies and total market cap has steadily decreased.

Source: Monetary Authority of Singapore website

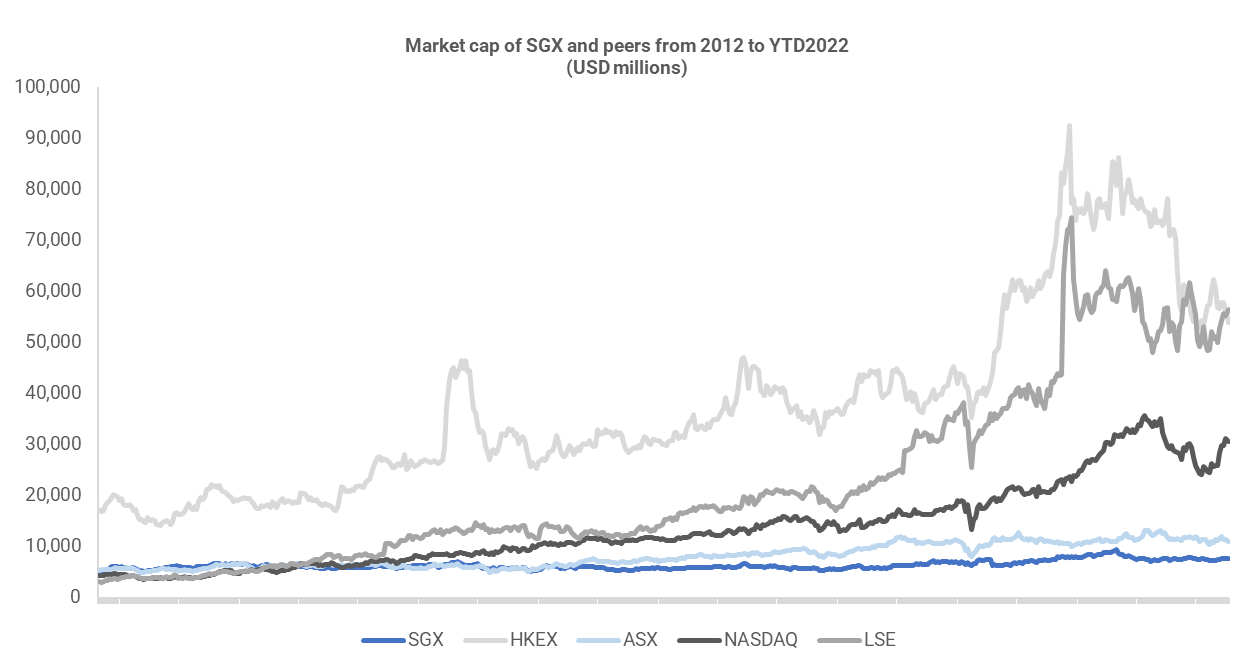

The consequence: the market cap of SGX that was higher than Nasdaq in 2012 has hardly progressed vs peers.

Source: Capital IQ

The cause of this slowdown is that the regulators have refused to go after fraudsters, whose dubious companies have been attracted by the environment of impunity. Noble is an example. It was listed in Hong Kong but moved to Singapore. Many hedge funds and investors gave up on investing in SGX-listed companies, because of this lack of enforcement. Valuation and liquidity declined. Companies that want to maximize their valuation choose not to list in Singapore as a consequence. It’s a vicious cycle.

SGX’s only solution thus far has been to pressure overseas-listed companies (e.g. Sea Ltd or Grab) to come back in the name of.. “national duty”. Yeah sure… What they call “national duty”, I call “bonus”.

Nobody is more outraged at the situation than Singaporeans themselves. The stock exchange is a perennial black spot in an otherwise successful finance center. But Singaporean journalists who did a fabulous job of reporting on Noble have less freedom to criticize regulators the same way. The media is controlled by the government.

Wirecard in Germany is another example of failed and conflicted regulators. There were however some journalists who were critical of how the regulators handled the fraud. The outcome? Wirecard CEO Markus Braun has been arrested and charged for fraud. Its COO Jan Marsalek is a wanted fugitive. German lawmakers have also called for an overhaul of the regulatory system.

Singapore’s regulators just don’t care. They can’t be criticized by the press. They can try to discredit whistleblowers. They are the unreachable elite. I have spoken to enough victims of this fraud, to know their anger over the way the regulators have handled this debacle is widespread. Who made money in this saga? The foreign fraudsters, the foreign auditor (E&Y). As for the regulators, they are very nicely paid for a highly questionable performance.

Who lost money? The multitude of retail investors left with nothing. They don’t matter. Their regulators won’t even try to recover their money. After years of the slowest investigation ever, they are happy to sweep the matter under the carpet with a meaningless fine. The regulators even show deference to the fraudsters when they refuse to name them in the public announcement. They have effectively shielded Noble’s crooks rather than protect their local investors.

The Singapore government shows no signs of wanting to change how its stock exchange is regulated. Wise investors will move their money elsewhere. And many Singaporean companies listed overseas will continue to dismiss the SGX as a potential venue for listing. Who can blame them?

It’s widely believed that prosecuting Enron’s management and reinforcing the regulatory environment strengthened capital markets in the US along with their competitive position. The Noble saga was an opportunity for the SGX to redeem itself. But its refusal to prosecute Noble’s fraudsters is the last straw for its already tarnished reputation.

Arnaud Vagner

Interpol red notice against former YuuZoo boss over misleading statements by company

Former executive chairman of YuuZoo, Mr Thomas Zilliacus, was in the news recently after he made a bid for Manchester United. PHOTO: BT FILE

Samuel Devaraj

FEB 21, 2024

SINGAPORE - A Singapore warrant of arrest and an Interpol red notice have been issued against the former executive chairman and chief executive of social media company YuuZoo, Mr Thomas Zilliacus.

They are over his alleged involvement in the release of misleading statements by the company, the Singapore Police Force (SPF) said in a statement on Feb 21.

The Finnish national, who is a Singapore permanent resident, was in the news recently after he made a bid for football club Manchester United.

The SPF said aside from Mr Zilliacus, three other individuals linked to the company – former chief financial officer Michael Parker, and independent directors Anthony Williams and Ozi Amanat – are also said to be involved in the same matter.

All four are currently out of Singapore and have refused to return, the SPF said. “Warrants of arrest have been issued against them. An Interpol red notice has also been issued against YuuZoo’s then CEO/executive chairman Thomas Zilliacus,” it added.

A red notice is a request to law enforcement worldwide to locate and provisionally arrest a person.

Earlier on Feb 21, the company’s former CEO James Matthew Somasundram, 59, was charged in court over misleading statements that overstated YuuZoo’s revenues by millions of dollars.

Somasundram was handed four charges over the making of misleading statements that were likely to induce the purchase of securities by other persons under the Securities and Futures Act.

Under the Act, an officer of a company is guilty of an offence when an offence committed by the company is proved to have been attributable to any neglect on the part of that officer.

The offences allegedly committed by YuuZoo are attributable to Somasundram’s neglect, the charge sheets stated. Somasundram was appointed CEO of YuuZoo – which is now known as YuuZoo Networks Group – on Oct 1, 2015, and stepped down in November 2016 for health reasons.

According to court documents for Somasundram, YuuZoo, which was listed on the Singapore Exchange (SGX) mainboard, allegedly made quarterly financial statements and dividend announcements that were released via the SGXNet Web platform in February, May, August and November in 2016.

Former YuuZoo CEO James Matthew Somasundram was charged in a district court on Feb 21 for the alleged offences that occurred in 2016. ST PHOTO: KELVIN CHNG

In the statements made for the fourth quarter of 2015, which were released in February 2016, the company was said to have overstated its revenue by US$18.8 million (S$25 million).

It was said to have overstated its revenue by $13.3 million in the statements made for the first quarter of 2016, and by $17.1 million in statements made for the second quarter of that year.

In the statements made for the third quarter of 2016, the company was said to have overstated its revenue by $8.9 million.

It is alleged that YuuZoo had known, or should have reasonably known, that the figures were misleading.

These alleged misleading overstatements were said to have likely induced other persons to purchase YuuZoo shares.

YuuZoo was co-founded in 2008 by Mr Zilliacus, who was CEO of the company before Somasundram. He resigned as chairman in April 2018 amid an investigation by the Commercial Affairs Department (CAD) into the company.

In a filing to the SGX, the company said the investigation was started after a complaint from an unknown party. It added: “While he (Mr Zilliacus) is convinced nobody in the company has done anything wrong, he has informed the board he believes the honourable thing to do is to step aside while the investigation is ongoing.”

The Business Times reported at the time that CAD was investigating the company for possible breaches of the Securities and Futures Act.

Somasundram is represented by Mr Adam Muneer Yusoff Maniam and Ms Gina Ding Huaxing from Drew & Napier. His next court date is on March 20. For each charge he faces under the Securities and Futures Act, he can be jailed for up to seven years, fined up to $250,000, or both.

Hyflux’s civil suits against founder Olivia Lum, ex-auditor KPMG to be jointly tried

The suits filed against Olivia Lum seek at least $690.6 million for alleged breach of fiduciary duty. PHOTO: ST FILE

Tay Peck Gek

MAR 25, 2024

SINGAPORE - Hyflux’s civil lawsuits against the company’s founder Olivia Lum and former auditor KPMG will be tried jointly, after the High Court granted Lum’s application for it.

Justice Goh Yihan, in a judgment published on March 25, said he agreed with Lum that a joint trial of the Hyflux claims will “save costs, time and effort, as well as promote convenience”.

“Crucially, the plaintiffs rely on the same pleaded facts in support of these causes of action… Similarly, the plaintiffs also claim to have suffered almost identical losses in both suits,” Justice Goh said.

KPMG supported the application for a joint trial because there are common questions of law and fact that arise in the suits.

Hyflux’s counsel had objected to having the claims heard before the same judge at the same time, arguing that there are a number of non-overlapping issues in both the suits that are key and substantial.

However, Justice Goh pointed out that the overlapping issues are key and substantial.

Beleaguered Hyflux and two subsidiaries, Hydrochem (S) and Tuaspring, as well as liquidator Cosimo Borrelli filed a lawsuit in 2022 against the group’s former chief executive Lum, seeking at least $690.6 million in claims over her alleged breach of fiduciary duty. Mr Borrelli is the liquidator of Hyflux and Hydrochem. He is not one of the three plaintiffs in the suit against KPMG.

Against KPMG, the two Hyflux companies and Tuaspring alleged that the professional services firm had breached its duty to exercise reasonable skill and care in carrying out its audit work in relation to its audit of the financial statements for 2011 to 2017, which were said to have been materially misstated. They are seeking over $684.6 million in claims.

High Court orders Falcon Energy to wind up after multiple failed restructuring attempts

Falcon Energy was ordered to wind up after the company had allowed the moratorium that was previously granted by the court to lapse. ST PHOTO: GIN TAY

Uma Devi

APR 05, 2024

SINGAPORE - Singapore’s High Court on April 5 issued a winding-up order to Singapore-listed offshore and marine player Falcon Energy Group, said the lawyers representing AmBank, more than five years after the company suspended the trading of its shares on the back of a debt overhaul.

Falcon Energy’s case was presided over by Justice Vinodh Coomaraswamy. AmBank, which is one of the company’s principal lenders, was represented by Hariz Lee of Joseph Tan Jude Benny, while Falcon Energy was represented by Anglo Law Chambers.

AmBank filed a winding-up order against Falcon Energy on Aug 25, 2021. Since then, both parties have been fighting it out in court, with Falcon Energy calling for the court to give it more time to restructure and AmBank putting pressure on it to either repay its debts to its creditors or wind up.

The Business Times understands that Justice Coomaraswamy ordered Falcon Energy to wind up after the company had allowed the moratorium that was previously granted by the court to lapse.

This was despite the company being reminded by the court on March 13 to file any extension application in sufficient time for it to be heard ahead of the winding-up hearing.

According to a March 27 affidavit seen by BT, one of Falcon Energy’s directors – Tan Sooh Whye – asked the court for the moratorium to be extended by two more months.

Ms Tan said the company faced difficulty in preparing the intended scheme of arrangement to be proposed to creditors, as well as the definitive agreements for the company’s proposed private placements, due to “cash-flow constraints”.

She argued that the company, in particular its marine division, is not currently trading as a majority of the group’s fleet of offshore support vessels have been sold. The only cash flow into the company has been monthly injections of various amounts from its directors, she added.

In written submissions filed by lawyers representing AmBank on Dec 13, 2023, it was noted that Falcon Energy has attempted to restructure itself three times.

In response to the company’s request for the first extension of the moratorium, AmBank’s lawyers opposed the application as they argued it was “not made in good faith”. They noted Falcon Energy’s director Tan Pong Tyea was the white knight investor of the company, and no other details of the purported investment had surfaced.

AmBank’s lawyers also flagged the lack of particulars pertaining to the identity of Falcon Energy’s white knight investors, as well as an “increasing disclosure” of unsecured creditors and the lack of future revenue. THE BUSINESS TIMES

Time to make it listed firms’ business to tackle undervalued shares to revive S’pore’s stock market

David Gerald

Persistent undervaluation and the absence of meaningful liquidity has seen the delisting of dozens of good-quality companies over the past 10 years. ST PHOTO: GIN TAY

APR 11, 2024

SINGAPORE – Calls to revive interest in local stocks have been growing in frequency over the past few years, stretching back to 2015, when 1,225 remisiers signed a letter of appeal written by the Society of Remisiers (SOR) to then Finance Minister Tharman Shanmugaratnam for urgent measures to restore confidence in Singapore equities.

Since then, Bloomberg news agency in 2019 described the Singapore market as “incredibly shrinking”, while in 2021, the South China Morning Post said the bourse’s “zombie” condition was undermining the Republic’s reputation as a financial hub, and perhaps more of a worry, added that the condition may be irreversible.

To its credit, the Singapore Exchange (SGX) responded by amending its listing rules to allow the entry of dual-class share companies and special purpose acquisition companies. Other initiatives include extending trading hours and the appointment of market makers.

However, SOR earlier in 2024 revisited its 2015 call for measures to “bring back the market’s glory days”.

Among the recommendations SOR made was to go for a “Big Bang”, that is, to list large government-linked companies such as PSA International and Changi Airport Group.

This is in the hope that the move would spark domestic interest in stocks as did the October 1993 listing of Singtel that not only gave Singaporeans a stake in the stock market but also triggered a “super bull run”.

The Singapore market performed admirably in the decade or so after Singtel went public but after the Straits Times Index reached an all-time high of around 3,907 in 2007, it has since floundered.

Today, it is estimated that of the 600-plus listed companies, less than a third trade above their book values. In comparison, more than 90 per cent of the S&P 500 trade above 1 time price/book value (P/BV).

Persistent undervaluation and the absence of meaningful liquidity has seen the delisting of dozens of good-quality companies over the past 10 years, often at sizeable discounts to fair value. This has understandably undermined confidence, prompting investors to look elsewhere for better opportunities.

What can be done? The Securities Investors Association (Singapore), or Sias, a shareholder activist group, believes that the problem has persisted long enough and agrees that it is time for everyone to take the bull by its horns (no pun intended) and to address the issue head-on with Sias’ three-pronged approach.

1. Take immediate steps to restore investor confidence

In conversations with brokers, loss of confidence is often cited as a key reason for the market’s lethargy.Retail investors are looking elsewhere after repeated blows. It started with the collapse of Clob International in the late 1990s, when Kuala Lumpur took action to end trading of Malaysian shares on the Clob platform.

This was followed immediately after by the S-chip debacle between 2000 and 2010, when the entire sector containing China companies crashed because of serious infractions of governance breaches and criminal offences.

Then there was 2013’s penny stock crash, when the regulatory authorities here intervened in the trading of three manipulated counters, resulting in a crash which wiped off $8 billion in market capitalisation.

The immediate priority should therefore be to address this issue. A proposal by SOR in 2022 to set up an ombudsman office to help retail investors seek recourse for investments that have failed through fraud or other possibly criminal actions would be a useful first step, as would swifter, sterner disciplinary action against errant directors.

In this connection, it is vital to raise the quality of directors to add confidence in boards. Sias earlier in 2024 recommended that the requirements to be a company director be tightened by requiring all new directors to be accredited by the Singapore Institute of Directors, something which is currently not the case.

Doing so will not guarantee that companies would be better run, but it would mean that boards at the very least possess the minimum qualifications and expertise to serve their shareholders properly.

2. Make listed companies take action if their shares trade below book value

One reason for investor unhappiness is that companies are being delisted at significant discounts to book value. When Sias challenges the initial prices, some companies respond with only a meagre upward revision, even though they could well afford a reasonably acceptable premium.Take, for instance, the privatisation offer by Isetan, where the offer price of $7.20 is a very generous 153.5 per cent premium over the counter’s last closing market price of $2.84 on March 28 prior to its announcement. In contrast, most other privatisation offers are at much smaller premiums over market prices, much to the disappointment of the minority shareholders.

The main reason why small shareholders accept lowball offers is the fear of ending up owning shares in an unlisted company. Instead of having this fear, minority shareholders should understand that they have the right to reject lowball offers and demand better prices.

In order to raise the confidence of small investors, one only needs to look to Japan for appropriate measures. In January 2023, the Tokyo Stock Exchange issued a report, “Summary of Discussions on Measures to Improve the Effectiveness of the Market Restructuring”, in which it correctly identified listed companies themselves as being primarily responsible for whether their shares are properly priced.

The report stated that at the time, about half of listed companies traded below 1 time P/BV, which then led to a new requirement for all firms whose shares persistently traded far below their book values to disclose measures they would be taking to address this undervaluation and to provide annual updates.

Another country whose authorities are looking to address persistent undervaluation is South Korea, where two-thirds of companies trade for less than 1 time P/BV, a phenomenon known as the “Korea discount”.

In February 2024, South Korea’s Financial Services Commission – obviously taking the cue from Japan – provided details of its “Corporate Value-up Programme”, which aims to prioritise shareholder returns through incentives, including tax benefits, and “encourage listed companies to voluntarily set up and disclose valuation enhancement plans”.

As far as South Korea is concerned, it is still too early to judge the effectiveness of the initiative, but in Japan, the measures have clearly been a spectacular success given the massive recovery in Japanese stocks over the past year.

Clearly, the local market would benefit from similar initiatives.

3. List large GLCs – and study the feasibility of GIC investing locally

Sias recommends the creation of a joint task force, possibly named a market strategy committee, to provide a multi-faceted approach to the issue of how to revive interest in Singapore stocks.Members of this body should, at the minimum, comprise representatives from the Monetary Authority of Singapore, SGX, SOR, the Securities Association of Singapore and Sias.

Apart from distilling the best of the measures adopted in Japan and South Korea for implementation here, other possible areas for study are the feasibility of not just listing large GLCs but also the sovereign wealth fund GIC investing in local companies, which is currently not the case.

If this were to occur, confidence and liquidity would surely improve, points that were made when the suggestion was first made back in 2016 by the Singapore Business Federation. Although at the time it received widespread support from the business and broking community, nothing further has been heard since.

Sias to ask about firms’ actions over undervalued shares

Sias, on its part, is studying the possibility of introducing a fourth question to its current “Three Questions’’, which are sent to hundreds of listed companies for them to answer before their annual general meetings (AGMs).The original three questions focused on the recipient’s financials, corporate strategy and governance, the answers to which have proven tremendously useful to all shareholders, not just those who subsequently attended the AGMs.

Sias’ hope is that the fourth question will target mainly companies whose shares trade below book values and will focus on steps managements and boards are planning to take to address this undervaluation.

Just as in the case of the Three Questions, answers to the Four Questions would be published either on company websites, or on SGX, or both.

If the above suggestions are favourably considered, it is Sias’ view that they will have an impact and should go some distance in reviving interest in the local market.

Similar threads

- Replies

- 3

- Views

- 554

- Replies

- 4

- Views

- 639

- Replies

- 4

- Views

- 400

- Replies

- 5

- Views

- 601