[h=1]GIC/CPF INVESTMENTS - ‘IDA TYPE’ DUE DILIGENCE?[/h]

Post date:

1 May 2015 - 2:02pm

Most of the reserves managed by GIC originated from CPF members, ie more than S$ 1/4 TRILLION. Billion$ in returns generated from past CPF investments were not returned to their rightful owners, CPF members. It’s therefore appropriate to refer to GIC’s investments as CPF investments.

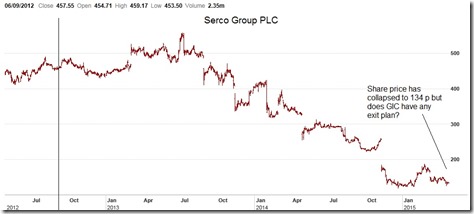

In an earlier post in December last year, I highlighted GIC’s S$260 million investment in Serco Group Plc, a UK company. Within 5 months, our CPF investment collapsed by 40%.

GIC appeared to be speculating with our CPF savings, trying to pick Serco’s bottom; its share price had almost halved from a year earlier. GIC’s due diligence seems to be similar to IDA’s.

Long-term Serco Group PLC chart

In another post in November last year, I questioned if there was an exit plan since Serco’s fundamentals had changed with the announcement of a £550m rights issue. But between face saving and tikam-tikam-and-hope-for-the-best, GIC chose the latter. GIC has no exit plan. Serco investment may be the nextLondon Mining where GIC had ‘buy high, sell low’. Only this time its strategy is likely to be ‘buy low, sell lower’.

According to the SWFI, GIC has participated in a 1 for 1 rights issue at 101 p , doubling its 35.17 million shares to about 70 million shares. In the latest rights issue, GIC has increased the investment by S$73 million (35.17 million X 101 p X 2.05), bringing the total Serco investment to about $333 million.

Serco has collapsed to about 134 p, which means GIC is sitting on paper losses of about S$140 million.

It appears GIC is speculating and when the investment has failed, throw good money after bad. No worries cause the $20 billion per year from our CPF tap will never run dry.

Changes in Serco’s fundamentals cannot be ignored as there are opportunity costs in holding onto an underwater investment.

To put it into perspective, global indices have been making new highs since 2013 but GIC has to pick a stock whose price had to decline by 63% (from 360 p to 134 p) in just 10 months? There are tens of thousands of stocks for GIC to choose from and picking on one hell of a loser is like striking Toto. In this case, CPF members will be giving away the Toto prize.

If GIC did not conduct ‘IDA type’ of due diligence, how did CPF members end up with Serco as one of our investments?

Phillip Ang

*The writer blogs at https://likedatosocanmeh.wordpress.com/

Post date:

1 May 2015 - 2:02pm

Most of the reserves managed by GIC originated from CPF members, ie more than S$ 1/4 TRILLION. Billion$ in returns generated from past CPF investments were not returned to their rightful owners, CPF members. It’s therefore appropriate to refer to GIC’s investments as CPF investments.

In an earlier post in December last year, I highlighted GIC’s S$260 million investment in Serco Group Plc, a UK company. Within 5 months, our CPF investment collapsed by 40%.

GIC appeared to be speculating with our CPF savings, trying to pick Serco’s bottom; its share price had almost halved from a year earlier. GIC’s due diligence seems to be similar to IDA’s.

Long-term Serco Group PLC chart

In another post in November last year, I questioned if there was an exit plan since Serco’s fundamentals had changed with the announcement of a £550m rights issue. But between face saving and tikam-tikam-and-hope-for-the-best, GIC chose the latter. GIC has no exit plan. Serco investment may be the nextLondon Mining where GIC had ‘buy high, sell low’. Only this time its strategy is likely to be ‘buy low, sell lower’.

According to the SWFI, GIC has participated in a 1 for 1 rights issue at 101 p , doubling its 35.17 million shares to about 70 million shares. In the latest rights issue, GIC has increased the investment by S$73 million (35.17 million X 101 p X 2.05), bringing the total Serco investment to about $333 million.

Serco has collapsed to about 134 p, which means GIC is sitting on paper losses of about S$140 million.

It appears GIC is speculating and when the investment has failed, throw good money after bad. No worries cause the $20 billion per year from our CPF tap will never run dry.

Changes in Serco’s fundamentals cannot be ignored as there are opportunity costs in holding onto an underwater investment.

To put it into perspective, global indices have been making new highs since 2013 but GIC has to pick a stock whose price had to decline by 63% (from 360 p to 134 p) in just 10 months? There are tens of thousands of stocks for GIC to choose from and picking on one hell of a loser is like striking Toto. In this case, CPF members will be giving away the Toto prize.

If GIC did not conduct ‘IDA type’ of due diligence, how did CPF members end up with Serco as one of our investments?

Phillip Ang

*The writer blogs at https://likedatosocanmeh.wordpress.com/