1. Increase the interest payable, but increase the minimum sum of 3% annually from 2017 to 2020

2. Choice of withdrawing the full sum comes 55.........

1The CPF Advisory Panel is recommending that members set aside a Basic Retirement Sum at 55, so that they can draw on a payout of S$650 to S$700 per month when they retire a decade on. It also proposed lump-sum withdrawals of up to 20 per cent.

The CPF advisory panel releasing their recommendations. (Photo: Imelda Saad Aziz)

SINGAPORE: The Central Provident Fund (CPF) Advisory Panel, chaired by Professor Tan Chorh Chuan, on Wednesday (Feb 3) submitted its first batch of recommendations to the Government on ways to enhance the CPF system to better meet the needs of Singaporeans in their retirement years.

There were a total of nine recommendations submitted, including the introduction of a Basic Retirement Sum, an additional lump sum withdrawal point when the member is 65 years old, and allowing members to defer their payout starting age.

Channel NewsAsia breaks down the key recommendations, and the implications on CPF members and their retirement planning.

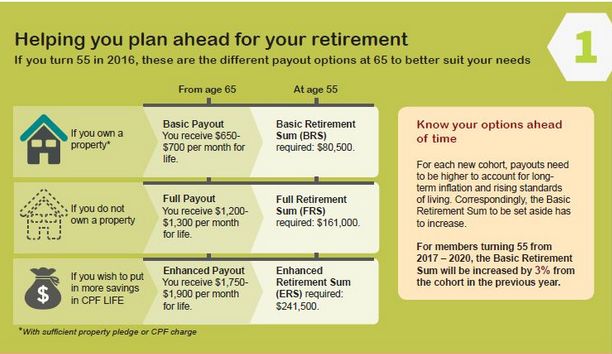

RECOMMENDATION: Members who retire in 10 years’ time should set aside CPF savings to provide for a monthly payout of S$650 to S$700, or Basic Payout. To receive this Basic Payout, members have to set aside a Basic Retirement Sum. This is with the assumption that the member owns a home and does not need to pay rent.

What it means: CPF members who turn 55 in 2016 can receive the monthly Basic Payout of S$650 to S$700 for their lifetime from age 65, if they set aside the Basic Retirement Sum of S$80,500, as a premium for CPF LIFE.

Those unable to meet the Basic Retirement Sum, but who have signed up for CPF LIFE, will still receive monthly payouts, but these amounts would be correspondingly lower than the Basic Payout mooted. They do not have to top up their Retirement Accounts with cash in order to be part of CPF LIFE.

For those who meet the Basic Retirement Sum and wish to withdraw savings on top of the S$80,500 set aside, they may do so subject to making a property pledge. This pledge is basically a commitment by the member to put back the amount withdrawn from the proceeds after the property is sold.

For those who have bought their homes using CPF, there is already a CPF charge on that property, so there is no need to make a property pledge. CPF will be able to tell from past transactions on their systems whether the member is eligible for a CPF charge.

But for others with no or insufficient CPF charge on their property, the property pledge rules still apply.

“It is expected that among the cohort of CPF members turning 55 in 2020, about 7 in 10 active members will be able to accumulate enough CPF savings to meet their Basic Retirement Sum,” the advisory panel said.

RECOMMENDATION: Those who do not own a home, or do not wish to pledge it, should set aside a retirement sum double the Basic Retirement Sum - also known as the Full Retirement Sum.

What it means: People who do not have homes to their name, or who do not want to pledge their property, will have to set aside S$161,000 in order to receive monthly payouts of between S$1,200 and S$1,300 from age 65.

RECOMMENDATION: Give the option to members with higher CPF balances to commit more of their savings into the CPF LIFE scheme, so they receive higher monthly payouts.

What it means: These members would be able to voluntarily top up their CPF LIFE to an Enhanced Retirement Sum, which is capped at three times the Basic Retirement Sum. In other words, those who turn 55 in 2016 can choose to top up their CPF LIFE amount up to the limit of S$241,500 to get higher monthly payouts.

This was previously impossible, as the Minimum Sum was also the ceiling with which members could annuitise - or convert into fixed monthly payments - their savings.

RECOMMENDATION: Give members the option to defer their payout start age, up to 70, for permanently higher monthly payouts.

What it means: According to the Ministry of Manpower’s Labour Force Survey in 2014, about 40 per cent of Singapore Residents between 65 and 70 continue to receive an income from work. Some members may not need their payouts to start at their Payout Eligibility Age (previously known as “Draw Down Age”).

Thus, the panel is proposing to incentivise these members to voluntarily defer their payouts in exchange for higher payouts. For every year the payment start age is deferred, monthly payouts permanently increase by 6 to 7 per cent. This will help more members with low CPF balances receive higher monthly payouts.

RECOMMENDATION: Give members the option to withdraw up to 20 per cent of their Retirement Account at the Payout Eligibility Age.

What it means: This option applies only to CPF members who turn 55 from 2013 onwards, since older cohorts had more liberal withdrawal rules at this stage. Those who turned 55 in 2008, for example, could withdraw up to 50 per cent of their combined Ordinary and Special Accounts.

Under this proposal, members will be able to withdraw up to 20 per cent of their Retirement Accounts, inclusive of the S$5,000 that can already be withdrawn unconditionally from age 55.

However, there is an impact on the monthly payouts if the member decides to withdraw the full 20 per cent at this stage. For example, if the member decides to not make the lump sum withdrawal at the Payout Eligibility Age of 65, and assuming there is S$80,500 in the Retirement Account, he or she will get to receive S$680 per month. Those who choose to withdraw the lump sum will have an estimated monthly payout of S$580.

“The panel proposes that the Government consider providing incentives to encourage CPF members, particularly those with low balances, to leave their retirement savings in the CPF if they have no urgent need to make a withdrawal,” it said.

ACCESS AND ASSURANCE

This first batch of recommendations addressed two of the four areas the panel members were charged to study:

•How the Minimum Sum should be adjusted after 2015, in order to meet the objective of delivering a basic monthly retirement payout for life

•How to enable CPF member to withdraw more as a lump sum upon retirement, and the circumstances for their doing so, taking into consideration the impact on retirement adequacy for different groups

Since its formation in September 2014, the panel met with more than 400 Singaporeans of various ages and different walks of life at its Focus Group Discussions.

“We noted the desire for more assurance over future adjustments to the Minimum Sum, and for there to be more choices in the CPF system for members,” Prof Tan, who is also President of the National University of Singapore (NUS), said in a letter to Manpower Minister Tan Chuan-Jin.

On the issue of lump sum withdrawal, he added: “We took into the account the desire expressed by many Singaporeans to have access to a portion of their savings for various uses, but were also mindful about keeping to the primary intent of the CPF system: To help provide retirement adequacy for the majority of Singaporeans.”

The panel is working on the second batch of recommendations, which they said will be submitted "later this year".

Said Professor Tan: "The key shift is that the most relevant sum or the base line for the majority of members will become the Basic Retirement Sum. This is because the majority of members own a property, and with this property they are able to take out sums above the basic retirement sum so long as they have a charge on their property.

“So let me explain what this charge is - when CPF members use their funds to buy a property, there's a charge on it. Which means when you sell that property, that amount is returned back to your CPF to ensure that you have adequate payouts in the future. This situation applies to the majority of CPF members."

2. Choice of withdrawing the full sum comes 55.........

1The CPF Advisory Panel is recommending that members set aside a Basic Retirement Sum at 55, so that they can draw on a payout of S$650 to S$700 per month when they retire a decade on. It also proposed lump-sum withdrawals of up to 20 per cent.

The CPF advisory panel releasing their recommendations. (Photo: Imelda Saad Aziz)

SINGAPORE: The Central Provident Fund (CPF) Advisory Panel, chaired by Professor Tan Chorh Chuan, on Wednesday (Feb 3) submitted its first batch of recommendations to the Government on ways to enhance the CPF system to better meet the needs of Singaporeans in their retirement years.

There were a total of nine recommendations submitted, including the introduction of a Basic Retirement Sum, an additional lump sum withdrawal point when the member is 65 years old, and allowing members to defer their payout starting age.

Channel NewsAsia breaks down the key recommendations, and the implications on CPF members and their retirement planning.

RECOMMENDATION: Members who retire in 10 years’ time should set aside CPF savings to provide for a monthly payout of S$650 to S$700, or Basic Payout. To receive this Basic Payout, members have to set aside a Basic Retirement Sum. This is with the assumption that the member owns a home and does not need to pay rent.

What it means: CPF members who turn 55 in 2016 can receive the monthly Basic Payout of S$650 to S$700 for their lifetime from age 65, if they set aside the Basic Retirement Sum of S$80,500, as a premium for CPF LIFE.

Those unable to meet the Basic Retirement Sum, but who have signed up for CPF LIFE, will still receive monthly payouts, but these amounts would be correspondingly lower than the Basic Payout mooted. They do not have to top up their Retirement Accounts with cash in order to be part of CPF LIFE.

For those who meet the Basic Retirement Sum and wish to withdraw savings on top of the S$80,500 set aside, they may do so subject to making a property pledge. This pledge is basically a commitment by the member to put back the amount withdrawn from the proceeds after the property is sold.

For those who have bought their homes using CPF, there is already a CPF charge on that property, so there is no need to make a property pledge. CPF will be able to tell from past transactions on their systems whether the member is eligible for a CPF charge.

But for others with no or insufficient CPF charge on their property, the property pledge rules still apply.

“It is expected that among the cohort of CPF members turning 55 in 2020, about 7 in 10 active members will be able to accumulate enough CPF savings to meet their Basic Retirement Sum,” the advisory panel said.

RECOMMENDATION: Those who do not own a home, or do not wish to pledge it, should set aside a retirement sum double the Basic Retirement Sum - also known as the Full Retirement Sum.

What it means: People who do not have homes to their name, or who do not want to pledge their property, will have to set aside S$161,000 in order to receive monthly payouts of between S$1,200 and S$1,300 from age 65.

RECOMMENDATION: Give the option to members with higher CPF balances to commit more of their savings into the CPF LIFE scheme, so they receive higher monthly payouts.

What it means: These members would be able to voluntarily top up their CPF LIFE to an Enhanced Retirement Sum, which is capped at three times the Basic Retirement Sum. In other words, those who turn 55 in 2016 can choose to top up their CPF LIFE amount up to the limit of S$241,500 to get higher monthly payouts.

This was previously impossible, as the Minimum Sum was also the ceiling with which members could annuitise - or convert into fixed monthly payments - their savings.

RECOMMENDATION: Give members the option to defer their payout start age, up to 70, for permanently higher monthly payouts.

What it means: According to the Ministry of Manpower’s Labour Force Survey in 2014, about 40 per cent of Singapore Residents between 65 and 70 continue to receive an income from work. Some members may not need their payouts to start at their Payout Eligibility Age (previously known as “Draw Down Age”).

Thus, the panel is proposing to incentivise these members to voluntarily defer their payouts in exchange for higher payouts. For every year the payment start age is deferred, monthly payouts permanently increase by 6 to 7 per cent. This will help more members with low CPF balances receive higher monthly payouts.

RECOMMENDATION: Give members the option to withdraw up to 20 per cent of their Retirement Account at the Payout Eligibility Age.

What it means: This option applies only to CPF members who turn 55 from 2013 onwards, since older cohorts had more liberal withdrawal rules at this stage. Those who turned 55 in 2008, for example, could withdraw up to 50 per cent of their combined Ordinary and Special Accounts.

Under this proposal, members will be able to withdraw up to 20 per cent of their Retirement Accounts, inclusive of the S$5,000 that can already be withdrawn unconditionally from age 55.

However, there is an impact on the monthly payouts if the member decides to withdraw the full 20 per cent at this stage. For example, if the member decides to not make the lump sum withdrawal at the Payout Eligibility Age of 65, and assuming there is S$80,500 in the Retirement Account, he or she will get to receive S$680 per month. Those who choose to withdraw the lump sum will have an estimated monthly payout of S$580.

“The panel proposes that the Government consider providing incentives to encourage CPF members, particularly those with low balances, to leave their retirement savings in the CPF if they have no urgent need to make a withdrawal,” it said.

ACCESS AND ASSURANCE

This first batch of recommendations addressed two of the four areas the panel members were charged to study:

•How the Minimum Sum should be adjusted after 2015, in order to meet the objective of delivering a basic monthly retirement payout for life

•How to enable CPF member to withdraw more as a lump sum upon retirement, and the circumstances for their doing so, taking into consideration the impact on retirement adequacy for different groups

Since its formation in September 2014, the panel met with more than 400 Singaporeans of various ages and different walks of life at its Focus Group Discussions.

“We noted the desire for more assurance over future adjustments to the Minimum Sum, and for there to be more choices in the CPF system for members,” Prof Tan, who is also President of the National University of Singapore (NUS), said in a letter to Manpower Minister Tan Chuan-Jin.

On the issue of lump sum withdrawal, he added: “We took into the account the desire expressed by many Singaporeans to have access to a portion of their savings for various uses, but were also mindful about keeping to the primary intent of the CPF system: To help provide retirement adequacy for the majority of Singaporeans.”

The panel is working on the second batch of recommendations, which they said will be submitted "later this year".

Said Professor Tan: "The key shift is that the most relevant sum or the base line for the majority of members will become the Basic Retirement Sum. This is because the majority of members own a property, and with this property they are able to take out sums above the basic retirement sum so long as they have a charge on their property.

“So let me explain what this charge is - when CPF members use their funds to buy a property, there's a charge on it. Which means when you sell that property, that amount is returned back to your CPF to ensure that you have adequate payouts in the future. This situation applies to the majority of CPF members."